MyBnk calls for 30 hours a year of financial education in UK schools

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

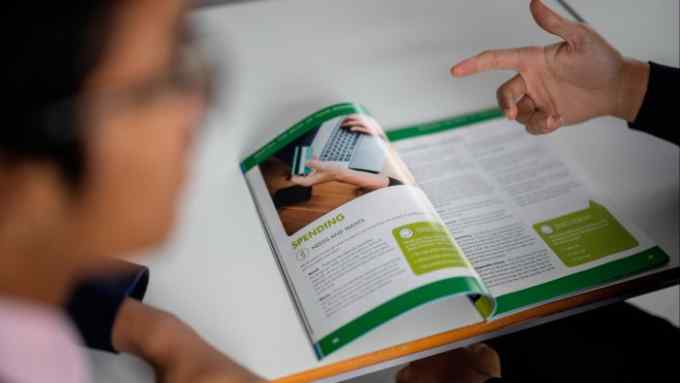

This article is the latest part of the FT’s Financial Literacy and Inclusion Campaign

Young people require a working week of tuition each year to be financially literate by the time they leave school, according to a new report.

MyBnk, the education charity which led the Money & Pensions Service’s financial workshops for 16 and 17-year-olds, said that 30 hours of financial education each year for 11 to 18-year-olds would significantly boost money management and practical maths skills.

These recommendations will be published in a report on Monday, alongside a financial education measure developed by the consultancy Centre for Economics and Business Research (Cebr). The new metric, based on survey data from February and March, shows that only 41 per cent of young people could be classified as financially literate.

Almost two-thirds of young adults do not recall having received financial education at school, according to Cebr. MyBnk’s chief executive, Leon Ward, said the government should explore expanding financial literacy outside the core curriculum to include extracurricular awards.

“We should think broadly about education, it can happen in the home between families and not just tied up with formal education and a controlled setting,” said Ward. Individuals would have responded better to inflation had they received formal training in money management, he said.

The current economic climate has sharpened the need for financial awareness among those struggling with debt and cost of living pressures.

Mark Bailie, chief executive of price comparison website Compare the Market, which funded the research, said a lack of financial confidence was impacting decision-making in households.

Several charities including the FT’s Financial Literacy and Inclusion Campaign (FLIC) and National Numeracy have pressed the government for proper provision of financial education. The CBI previously estimated that prioritising financial education would boost the UK economy by £6.8bn each year.

“Teachers and parents have a lot of pressures on their time, so FT FLIC has prioritised the creation of easy-to-use educational resources on basic finance,” said Aimée Allam, FLIC’s executive director.

In February the all-party parliamentary group (APPG) for financial education said schools were struggling to teach financial education despite it being a mandatory part of the national curriculum. It said budget and training requirements were a barrier to teaching finance.

A survey of teachers commissioned by the APPG found around half of all respondents said they had no ring fenced budget for teaching financial education in their school.

Allam added: “We would welcome an explicit endorsement from the government about the importance of financial education to help empower the next generation to navigate an increasingly complex economic landscape.”

Comments