Best of FT Money 2021: Why financial literacy is a passport to financial freedom

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Like a Bat out of Hell pounds from a ghetto blaster outside one of the small terraced houses on Beaumont Street. For the couple and their two children who sit on garden chairs in the potholed road listening to it, this is what passes for entertainment in the most deprived part of the most deprived town in England. A few yards away, a man staggers from an off-licence, barely able to stand at 3.30pm.

This is the North Ormesby area of Middlesbrough, a few miles from England’s bracing but beautiful north-east coast. Years of deindustrialisation (the Teesside area’s iconic steelworks is in the midst of a year-long demolition) and low educational achievement (Middlesbrough’s A-level attainment rate is half the national average) have by several measures kept the area at the top of the charts of England’s most economically deprived local authorities.

For much of the UK — like much of the developed world — the ravages of Covid and the privations of lockdown did not cause economic stress. Indeed, the wealth of UK households increased by nearly £900bn, according to the Resolution Foundation. But that overall picture hid a widening of the wealth gap, as those with assets and jobs benefited, and those with low incomes fell further into debt.

About a third of those who were out of work, furloughed or had their pay cut during the pandemic dipped into their savings, the Resolution Foundation research found. More than 20 per cent of the same categories increased borrowing.

Val Gibson, a much-loved maternal figure who runs the North Ormesby Community Hub, has seen that kind of fallout every day. “With the financial losses that they’ve suffered recently [during Covid], and especially with the £20 a week of state benefits that they’re going to lose [as the Covid period top-up falls away], families here are suffering,” she says.

“Their biggest worries are debt and housing and generally managing on their money. Many people just spend their [state] benefits as soon as they get them, they don’t budget.”

Fixing economic deprivation is a mammoth task, but assisting with basic financial education — to boost budgeting skills, debt knowhow and investment nous — need not be. And yet basic financial understanding can make a vast difference — not just to poorer communities such as North Ormesby, but to anyone in virtually any circumstance.

“Improving financial capability can be transformative for individuals and families,” says Diane Maxwell, former lead of New Zealand’s state-backed financial capability drive. “People report better sleep, feeling more in control, greater family cohesion, and are more likely to think long term. In that sense it has a powerful upward momentum to it.”

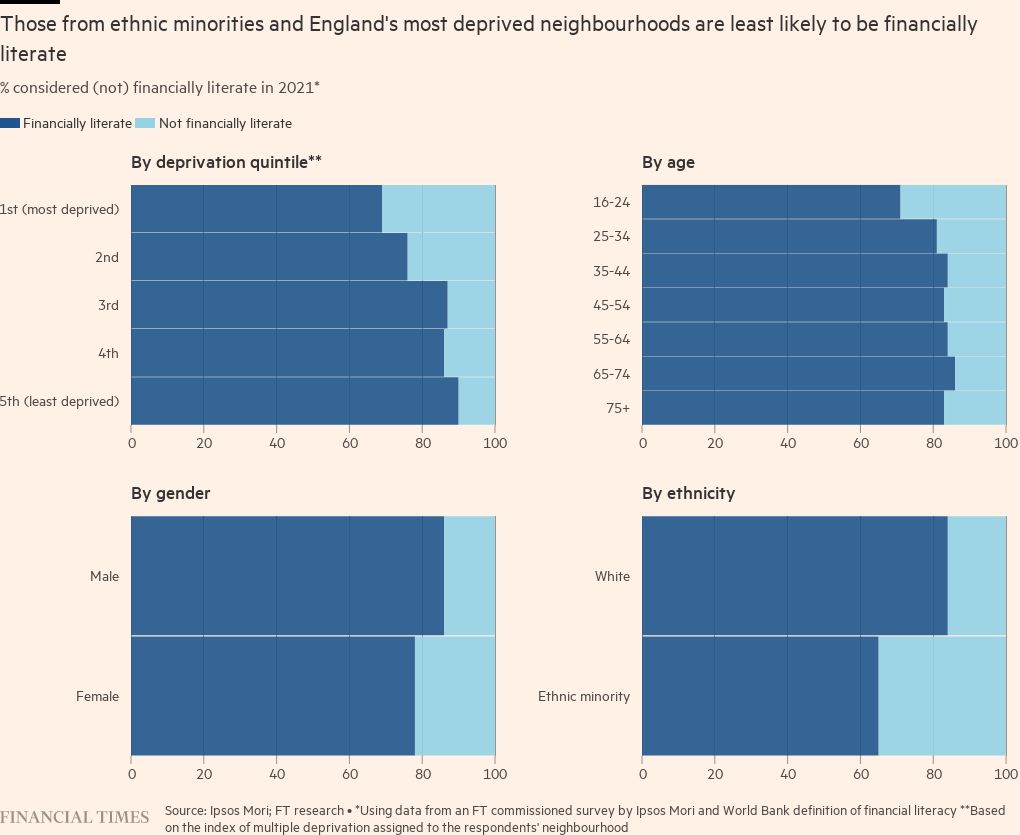

New survey data, commissioned for the Financial Times from Ipsos Mori, reveals striking shortcomings in financial understanding that cement inequality. The research, undertaken as the FT launches its own charitable venture, the FT Financial Literacy and Inclusion Campaign (FT FLIC), identifies four constituencies that have clear gaps relative to the national average: deprived areas, the young, women and ethnic minorities.

FT FLIC’s Strategic Vision, published today, outlines its plan to boost financial literacy in the UK and around the world through a campaign of financial education, targeted at young people, women and the disenfranchised.

The correlation between high levels of economic deprivation and low levels of financial understanding is one of the starkest. The FT Ipsos Mori research in England suggests that already vulnerable communities find their problems worsened by low levels of knowledge about how debt interest is calculated, how it compounds and how to mitigate risk or budget effectively.

But the other groups with financial literacy shortcomings answered questions on those subjects with similarly low scores. Asked, for example, whether (a) £105 or (b) £100 plus 3 per cent interest was the lower sum to repay on a £100 one-year loan, only 72 per cent of those living in the most deprived fifth of English neighbourhoods knew the answer was (b), compared with 86 per cent of those living in the best-off areas. The tally for women was 77 per cent, ethnic minorities 66 per cent and 16-24 year-olds 69 per cent.

Many young people were also uncertain when asked an inflation question. Less than half of 16-24 year-olds knew that the value of your money would be eroded if it earned 1 per cent and inflation was running at 2 per cent. The overall tally knowing the right answer was 77 per cent, including 71 per cent of women, 63 per cent of those living in the most deprived neighbourhoods and 60 per cent of ethnic minorities.

Some questions proved a leveller for all. Asked to compare the relative cost of borrowing on a credit card and through a bank overdraft with specific charges, barely half got the right answer — virtually regardless of wealth bracket, age, ethnicity, region or gender. We could all do with a financial literacy boost.

Indeed, judged on the core financial literacy questions in the Ipsos Mori survey — some of which mimic a global study conducted by Standard & Poor’s Ratings Services seven years ago — the population as a whole has little cause to be sanguine. Just over one in five respondents answered all these questions correctly.

From the 2014 S&P Global FinLit Survey, only a third of the world’s population were deemed financially literate, according to analysis by the World Bank, based on getting three of five very similar questions right, including one of those on compound interest. The UK tally was 67 per cent. (Although on the same basis the English financial literacy score in the FT-Ipsos Mori poll was 82 per cent, experts believe that is likely to reflect the change from telephone to online polling, rather than a substantial underlying national improvement.)

“Low incomes and poverty are too often compounded by under-regulated markets, inaccessible language and limited financial understanding,” says Aimée Allam, executive director of FT FLIC. “Narrowing the financial literacy gap is crucial for narrowing the wealth gap. But financial literacy clearly needs a boost across the social strata too.”

It is precisely that mission that the new FT FLIC charity is taking on — first in the UK, with a strategic plan published today, before expanding over time around the world. It will develop educational programmes to boost the financial literacy of young people, women and disadvantaged communities, and campaign for policy change and clearer product communication by financial companies.

Leanne Fielden fits the bill for the disadvantaged. She is an unemployed woman living in the deprived Middlesbrough region. I meet her at a free-to-attend exercise class put on by Middlesbrough Football Club’s charitable foundation. Like the dozen or so other women who are doing bench presses, battle ropes and squats in the wide corridors beneath the terraces at the Riverside Stadium, she raves about the community spirit fostered by health co-ordinator Paul South and his team of coaches. “This is something that gets me out without financial stress,” says Fielden, adding that she has lost 10 stone (63.5kg) in weight, partly thanks to the programme.

Her profile belies her own financial expertise. “I’m fortunate that I’ve worked for Barclaycard and Visa. I often help family and friends with money issues,” she says. So she herself has no fear of finance. “But I’ve got a fear of finance for the younger generation,” she says, adding that she’s convinced there is a solution. “One thing I honestly think should be taught in schools is finance. Too many children, my kids included, think money grows on trees. They don’t realise that they have to budget all this money as they get older, they’ve got to pay these bills. I was one of them. My mam and dad gave me everything. Mam died when I was 17 and I ended up moving abroad to work. And it was such a hard lesson for me. I didn’t know how to cook, how to clean, how to iron, I didn’t know how to look after my finances, it was really hard. It should be one of the things that’s taught to prepare them for the real world.”

Although financial literacy theoretically has a place on the national curriculum in England and other parts of the UK, it is often neglected. Some teachers blame a lack of time to teach it alongside health, citizenship, sex and relationships in so-called PSHE lessons. Others admit to a fear of finance themselves, meaning they do not prioritise it.

Poppy Train, a teenager who also attends the MFC Foundation fitness class, has seen that lack for herself. “We learn about simple interest and compound interest, but nothing more,” she says. Her mother Emma says she and her daughter both think “100 per cent” that it should be properly taught at school. “They [teachers] need to show the realism — get in a shop situation, say, so the kids realise how to budget.”

According to the FT-Ipsos Mori research, 90 per cent of the 3,194 people polled across England learnt “nothing at all” or “not very much” about finance at school.

Alongside providing financial educational content for individuals and teachers, FT FLIC plans to lobby for education policy to change, in particular pushing for financial literacy to be properly integrated into school curricula, rather than just an afterthought in PSHE lessons.

As Fielden says: “It’s something that’s going to benefit them more than doing some of the lessons they have to do curriculum-wise . . . My daughter is going into her GCSE years and she has to do French. Now I understand French is a good language, but unless she’s going to go to France, she isn’t ever going to need it, whereas finance, she’s always going to need it.”

One of the big reasons to target young people is that later in life they become much harder to reach. Back at the North Ormesby Hub, community leader Val Gibson is under no illusions about that: “We’ve run budgeting skills courses. But the ones who really need it won’t come in, unless you’re giving them something.” The desperate proof — dozens of gift bags filled with a few toiletries, Covid tests and word searches — lies strewn across her desk awaiting the next inducement effort.

Marc McPhillips, a manager at the MFC Foundation, has found his outreach work similarly challenging in the most deprived communities of nearby East Cleveland, once a rich source of iron for the region’s rapidly declining steel industry. “This is the land that time forgot, in terms of unemployment, poor education, bad public transport. And there was real mistrust when we arrived,” he says. Thanks to a former hedge fund manager who returned to his local area, and pledged generous (but anonymous) financing, the foundation became a crucial lifeline during the depths of Covid, providing food parcels and school meals as well as sports sessions and a “Boro Bus”, equipped with mobile health and exercise facilities. They have even stretched into ad hoc financial education, partnering with a local credit union.

One of FT FLIC’s approaches will be to partner with existing charities and other organisations in financial education, becoming a hub for the aggregation of the best existing material, as well as developing its own content.

If financial literacy education can be instrumental in helping the most deprived to improve their lot, it can be similarly transformational for other groups that lack basic foundational knowledge — to avoid financial dangers and improve their lives in aspirational ways.

Aside from being impressive football players, the 80 individuals who take part in the weekly games for asylum seekers organised by Paul South and his colleagues at the MFC Foundation have triumphed over adversity — battling their way to Britain from 25 different countries, from Afghanistan to Sudan and Cameroon, and surviving torture, persecution and economic stress. They remain inspiringly full of aspiration.

Rene Perez is from El Salvador, where his family fled the increasingly authoritarian regime in 2019. The 27-year-old is frustrated by the subsistence existence of the asylum seeker and is eager to build a new life. “I can’t work but I’ve been studying English skills and maths at Middlesbrough college. I want to get a career at college and work in construction. I like skyscrapers. I’d like to [operate] a crane.” I ask him what motivates him. “One of my dreams is to buy a flat in Manchester, especially in Salford close to the Old Trafford stadium. Really nice. One of my dreams. But I will need to save.” I explain to him the rudiments of how to accumulate a deposit and take out a mortgage loan. He looks incredulous at the idea that he wouldn’t have to save the entire amount to buy a property, but that once he has a decent job his dream may actually be achievable with a deposit and loan secured on the property. “I can borrow? I will have to be responsible.”

Financial literacy education, done right, can as much be a source of emancipation for refugees establishing themselves in their adoptive country as for the economically disadvantaged seeking a way out of deprivation. Targeted at the young, in particular, it can lay down vital foundations for future prosperity — aiding people on to the property ladder, teaching them about risk and investment opportunity. Financial literacy, quite simply, is a prerequisite for financial freedom.

Data analysis by Chelsea Bruce-Lockhart and John Burn-Murdoch

Patrick Jenkins is the FT’s deputy editor, former financial editor and chair of FT FLIC

Comments