India’s NSE set to take Hong Kong’s spot among world’s largest markets

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

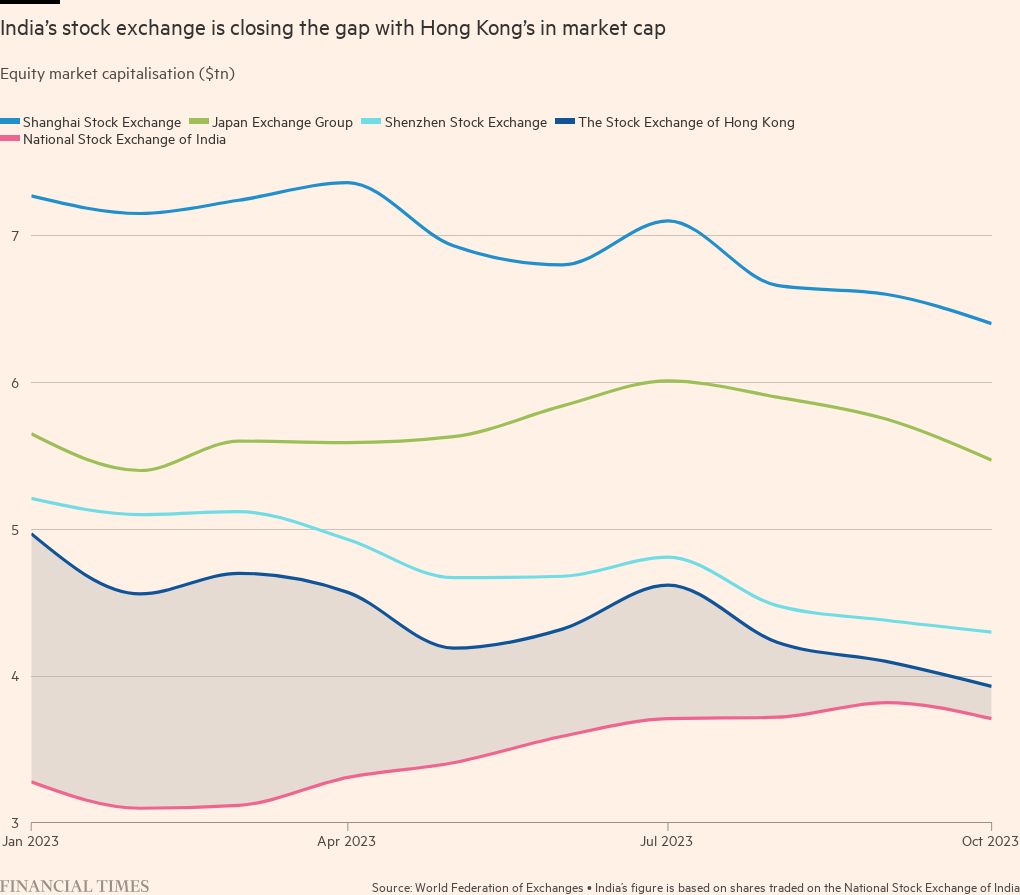

The value of the National Stock Exchange of India is poised to take Hong Kong’s spot among the world’s largest trading venues, in a rise analysts say attests to investors’ optimism about the economic prospects of the world’s most populous country.

The total market capitalisation of companies listed on the NSE was $3.7tn as of the end of October, according to the World Federation of Exchanges, a trade association of publicly regulated stock markets, compared with the Stock Exchange of Hong Kong’s $3.9tn.

Since that data was produced Indian share prices have surged further as a result of strong earnings and optimistic growth projections, putting it on track to become the world’s seventh largest after markets in the US, China, the EU and Japan.

Meanwhile share prices in Hong Kong have fallen as China’s economy cools.

India’s Nifty 50 index of large companies has risen 8.1 per cent over the past month, hitting record highs this week, while Hong Kong’s Hang Seng index fell 6.7 per cent over the same period, dragged lower by a liquidity crisis in the property sector and low investor and consumer confidence.

Over the past decade, India and China stock indices had “moved pretty much hand in hand” as part of an overall emerging markets story, said Abhiram Eleswarapu, head of India equities at BNP Paribas in Hong Kong.

They began diverging in the past three years, said Eleswarapu. “The China stock indices have generally been downward . . . whereas the India one has been going one way, which is up.”

Strong consumption in India is attracting investors, Eleswarapu said, pointing to increased spending on property, luxury and higher-end goods by affluent Indians, as well as growing government capital expenditure on infrastructure.

India is the world’s fastest-growing big economy this year, set to expand by 6.3 per cent this year, compared with 5 per cent for China, according to the IMF.

“When you look around the world, there aren’t that many countries where for the next 15-20 years you can be reasonably confident that you will see real GDP growth of at least 6 per cent on a sustainable basis,” said Pratik Gupta, chief executive and co-head of institutional equities at Kotak Securities in Mumbai.

Narendra Modi’s Bharatiya Janata party won three out of five recent local assembly elections in battleground states, boosting speculation that the ruling party will easily prevail in next year’s national election and maintain political and policy stability.

Indian companies are continuing to deleverage, a process that has been going on for several years, said Gupta. They have been paying down their debt and issuing equity in a trend that accelerated during the pandemic. Tata Technologies, a subsidiary of the Tata Group conglomerate, had a strong market debut in November, raising Rs30.4bn ($365mn) in an IPO that was subscribed 69 times.

India is also a beneficiary of the “China plus one” shift of supply chains away from China. The Financial Times reported this week that Apple, which has the bulk of its current manufacturing base in China, has asked component suppliers to source batteries for the forthcoming iPhone 16 from Indian factories.

Meanwhile, Tesla has held talks with Modi government officials about the possibility of setting up an Indian factory to make electric cars.

India’s rising share prices have been driven more by domestic than foreign money flows for most of this year. Foreigners are now net buyers of Indian equities, after being net sellers in September and October.

“China continues to underperform, and there are relatively few alternatives for investors who are focused on emerging equities,” said Deepak Jasani, head of retail research at HDFC Securities in Mumbai.

Comments