Central banks set to lift interest rates to 15-year highs as investor jitters grow

Simply sign up to the Central banks myFT Digest -- delivered directly to your inbox.

Leading central banks are due to raise interest rates this week to the highest levels since the financial crisis, stoking anxiety among some investors that this month’s bond market rally underestimates evidence of persistent inflation.

Bond prices have rapidly rebounded since the start of the year from last year’s historic sell-off, as markets bet that interest rate rises will slow and, in the case of the US Federal Reserve, even go into reverse. But some investors have doubts.

“I think it’s just a matter of the market kind of waking up to what the macro environment really is, as opposed to what they hope it is,” said Monica Erickson, head of investment grade credit at DoubleLine Capital. “[It] is going to be super difficult again for the Fed to . . . get inflation down to that magical 2 per cent number without putting us into a recession.”

Maureen O’Connor, global head of high-grade debt syndicate at Wells Fargo, said: “The credit markets are effectively pricing in a no-recession outcome. But that’s not the consensus base case that most economists are forecasting.”

A Bloomberg index tracking high-grade and junk-rated government and corporate bonds around the world has returned 3.3 per cent so far in 2023, putting it on course for its strongest January since its inception in 1999. Inflows into US and western European corporate bond funds are set for their best January on record, totalling $19.3bn up to January 26, according to EPFR data.

The Fed, the European Central Bank and the Bank of England will all hold policy meetings this week. Investors expect the Fed to slow the pace of its monetary tightening to 0.25 percentage points, raising rates to the highest level since September 2007, the start of the global financial crisis.

The BoE and the ECB are widely expected to lift rates by half a percentage point to their highest levels since autumn 2008 when Lehman Brothers filed for bankruptcy.

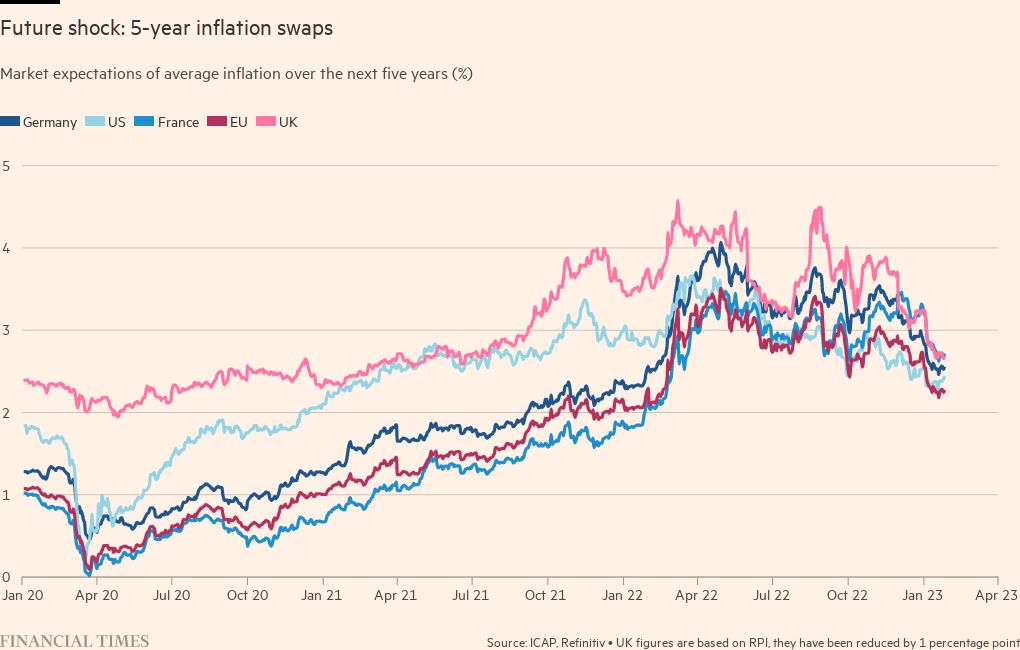

There are growing indications that underlying price pressures are proving persistent in the face of these rapid and globally co-ordinated rate rises — and the gap between investor expectations and economic data is widening.

Market measures of inflation suggest traders now expect inflation to eventually fall close to the Fed and ECB targets of 2 per cent. But price growth still stands at 6.5 per cent in the US, and 9.2 per cent in the eurozone. Core inflation — which omits volatile food and energy costs and is closely watched by central bankers — remains strong.

Consumers and businesses in most advanced economies expect inflation to remain higher than central bank targets in the medium term despite recent declines, surveys show. Policymakers closely watch such indicators, as well as market-based measures of expectations, because they can feed wage demands, fuelling further inflation.

“Inflation expectations can be a self-fulfilling prophecy, as higher expectations trigger the inflationary conditions that are envisioned,” said Nathan Sheets, chief economist at US bank Citigroup. Central banks’ concern was “ensuring that inflation expectations don’t ratchet upward from here”.

Jennifer McKeown, chief global economist at Capital Economics, said that “on almost all measures, inflation expectations are still much higher than their pre-pandemic levels and above the levels that would be consistent with the major banks’ 2 per cent inflation targets”.

If central banks keep rates high for a protracted period or raise them by more than investors expect, the bond market rally could unravel.

Yields on 10-year US Treasuries, a benchmark for borrowing costs across the globe, have slipped to 3.5 per cent from 3.9 per cent at the end of December. That has boosted the appeal of corporate bonds, which typically offer higher returns than their government counterparts.

Credit spreads — the premium that investors demand to hold corporate bonds over high-grade government debt — have narrowed since the start of January. The gap in yields between US investment grade debt and Treasury notes has tightened by 0.1 percentage points so far this year.

Spreads on lower-rated high-yield bonds have tightened even more, losing almost 0.6 percentage points.

“The investment grade market is pretty priced for perfection right now,” said O’Connor. “I worry about the black swan events and the catalysts that could catapult spreads wider from here.”

Such concerns have not stopped a wave of cash pouring into bond markets.

“There is a lot of money chasing yields,” said Rick Rieder, chief investment officer for fixed income at BlackRock. “In an environment where growth is slowing, where the equity market is not appealing, people are saying — there is an attractive yield and I can lock this rate up.”

Comments