Are structured products to blame for suppressed volatility?

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

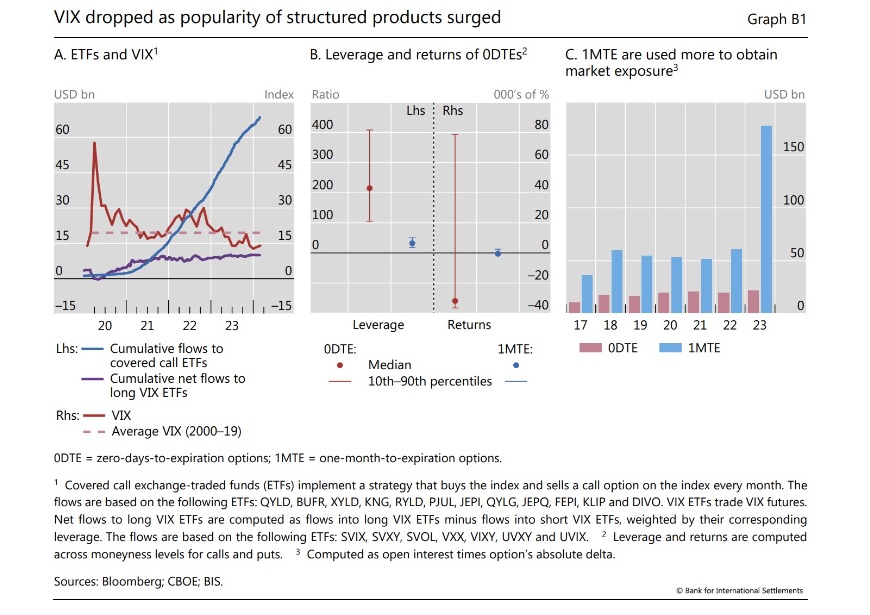

For a while now, people with too much time on their hands have argued that the Vix index is too low. Some attribute this to the surge in zero-day options trading. The Bank for International Settlements has another theory.

Yes, we’re dipping back into the BIS quarterly review. Yesterday Alphaville dug into its aside on prime brokerages, but the report also contained an interesting breakout box on the volatility index’s mysterious quietude.

The BIS doesn’t disagree that so-called 0DTEs have become wildly popular, noting that they accounted for over half of all SPX options trading volume in August 2023, up from only 5 per cent in 2016. The attractions are the immense leverage and massive payoffs that are possible from these quickfire lottery-ticket options, which as the name implies expire at the end of the day they’re bought.

While the annualised returns of 0DTE options is -32,000 per cent (!!!) they can “on rare occasions” generate returns of up to 79,000 per cent (!!!!!), the BIS calculates. Meanwhile, boring old monthly options only have an average annual return of -550 per cent and a maximum payout of 2,500 per cent, according to BIS. How would you even know you’re alive with those?

However, the BIS’s Karamfil Todorov and Grigory Vilkov are sceptical that the migration of investor interest away from one-month options to daily ones explains the decline in the Vix, which uses one-month options to calculate its spot level.

To blame instead is the rising demand for structured products built by investment banks and sold to yield-hungry investors, Todorov and Vilkov argue.

This is because of dealer hedging to limit exposure to sudden market moves. Alphaville’s emphasis below:

An alternative and presumably more likely reason behind the compression of volatility is the surge in issuance of yield-enhancing structured products. These types of structured products provide a yield enhancement by offering higher returns to investors thanks to the sale of options.

A classic example of a yield-enhancing structured product is a so-called “covered call”: a purchase of the S&P 500 index and a simultaneous sale of a one-month call option on the index. The product gives an exposure to the index and generates a yield enhancement with the sale of the call option (the premium income), but it gives up part of the upside if the index rises above a threshold, say 5% over the next month. In other words, an investor in this covered call effectively takes the view that the market will not rise more than 5% over the next month and monetises this view by selling the call option. A covered call is just a simple illustration of a yield-enhancing structured product, but there are many more-complicated types. These structured products are frequently offered to retail investors by banks, which are often dealers.

The rise of yield-enhancing structured products may dampen volatility due to the mechanics of how dealers hedge option exposures. When dealers sell such structured products, they effectively buy an option from their clients. To hedge the option exposure, dealers trade in the underlying asset (the equity index) as a function of its price. Specifically, they need to buy when the index goes down and sell when it goes up – a practice known as “dynamic hedging”. By doing so, dealers act in a contrarian way, effectively dampening the price movements of the underlying asset. As volatility declines, so does the cost of ensuring against it, as reflected in option prices.

Such market dynamics could explain why the VIX can be depressed even in an environment of heightened uncertainty. Suggestive of this mechanism at play, the meteoric rise of yield-enhancing structured products linked to the S&P 500 over the last two years has gone hand in hand with the drop of VIX over the same period.

You can see what they mean in the right-hand chart below (zoomable version):

It seems very plausible that this is “a” factor, but it’s long been known that dealer hedging mostly suppresses volatility (up to a point!). And it’s obviously not a case of either/or. Those structured product flows are eye-catching, but are they alone big enough to warp the options market, and the Vix with it?

Anyway, the idea that the Vix was somehow “broken” was more of a discussion in 2022, when it stayed somnolent despite US equities entering a bear market. Now that stocks are ripping higher, it doesn’t stand out as much.

Further reading:

— An oral history of the fear index (FTAV)

{kind=link}

Comments