Falling inflation might not dent gold’s rally

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is a former chief investment strategist at Bridgewater Associates

The latest US inflation data has reinforced market expectations that a Goldilocks-style soft landing will emerge in the year ahead, with the Federal Reserve able to ease monetary policy despite a relatively strong labour market.

In such a scenario, it would be reasonable if investors favoured stocks and even bonds over gold. Historically, zero-yielding gold has tended to perform better in the “tails” of the economic-cycle bell curve, either into a recessionary environment with low and falling interest rates and elevated uncertainty or an environment of economic overheating with high and rising inflation.

Looking at the year ahead, however, there are at least three factors that could help gold keep its lustre, even if hopes of a soft landing are realised. Central banks suggest they intend to add more gold to their reserves, and China’s central bank in particular has room to do so. In addition, the ongoing property deleveraging in China, weighing down on the country’s economy and domestic assets, may keep Chinese households looking to gold as a preferred store of wealth. Finally, investors broadly may want to increase gold allocations as a hedge against an unusually busy political calendar that could exacerbate an already unsettled geopolitical backdrop.

First, on central banks and gold, it is important to remember that reserve assets are chosen mainly for liquidity and stability, rather than returns. That is a key reason why central banks own so many US government bonds. Recent years have elevated another priority for central banks, however — diversification to protect against geopolitical shocks. Russia’s annexation of Crimea in 2014, and then the 2022 war in Ukraine, resulted in an increasing number of western sanctions on Russian assets, including its central bank reserves. This triggered a renewed focus on reserve diversification, especially by Russia and countries doing business with it. They wanted to shift reserves away from US dollar-denominated assets, as well as from assets of US allies that might be inclined to implement similar sanctions.

Gold benefited. It provided a relatively liquid, stable asset that could be used outside global payment systems (notably Swift) and historically had performed well in periods of heightened uncertainty. In 2022, central banks purchased a record 1,136 tonnes of gold, according to the World Gold Council, with another 800 tonnes bought in the first three quarters of 2023. Gold buying was led by emerging economies, notably China and Turkey.

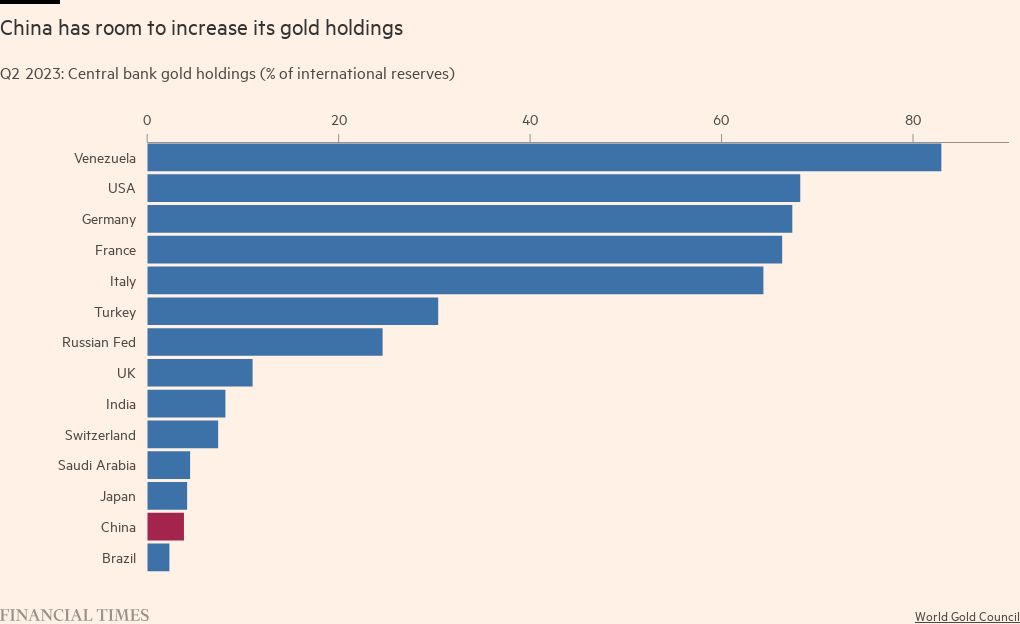

China has been the largest buyer of gold for central bank reserves this year by far with purchases of 181 tonnes in the nine months to September 30, taking total holdings to 2,192 tonnes. But it has ample room to increase gold holdings if it wants to further diversify. Gold represents around 4 per cent of its total reserves, near the low end of allocations by larger central banks.

For comparison, Russia’s gold reserves are just under a quarter of the country’s total, while Turkey’s gold represents 26 per cent of total reserves. The US and Germany have about two-thirds of total foreign reserves in gold. A survey by the World Gold Council released in May found that two-thirds of emerging economy central banks and 39 per cent of developed economy central banks expected to increase gold holdings over the next five years — to 16 per cent or greater as a share of total reserves. That would be a multiple of China’s current allocation.

In addition to China’s central bank, the country’s households, historically the world’s largest gold consumers, may be motivated to buy more. The country’s closed capital account and less developed financial markets limit ways to manage wealth. Historically, households have looked to housing, local equity markets and bank deposits. If the government is unable to sustainably stabilise property prices, the broader economy and equity market are likely to keep struggling. Against that backdrop, it seems reasonable that household savings may migrate more into gold in an effort to preserve wealth.

Finally, gold could play a larger role in 2024 as investors broadly hedge against macroeconomic and geopolitical risk. The year ahead brings elections in dozens of countries; more than half of the global population will be deciding on their leaders. Outcomes have the potential to trigger stark policy shifts in critical countries, including in the US, Taiwan and Mexico. These votes also may exacerbate geopolitical uncertainty, with the potential to weigh down on growth expectations and drag soft-landing hopes towards a more gold-friendly economic “tail”.

Comments