A shock looms for governments over inflation-linked bonds

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is founder and editor of Risky Finance

As inflation becomes more persistent across developed nations, there is a costly bill looming for governments.

In recent years, governments have exploited rising investor demand for bonds with returns that are linked to inflation, issuing increasing amounts of such instruments. The terms were attractive for issuers, with investors willing to accept negligible yields while inflation was low.

But now the bill to issuers is rising as inflation surges. An example of this can be seen with the UK, which pioneered this form of bonds, known as “linkers”, in the 1980s and is struggling to restore fiscal credibility after its abortive “mini” budget in September.

The UK’s Office for National Statistics has flagged the rising cost of linkers, noting that index-linked gilts accounted for £55bn of the UK’s £92bn interest payment bill in the year to August — an outsized contribution considering that they are 25 per cent of outstanding gilts.

Meanwhile, the US is set to pay $150bn in interest this year on its portfolio of Treasury inflation-protected securities, half the amount it pays on nominal Treasury bonds, according to the US Treasury website. This is even more remarkable, given that just 9 per cent of US government bonds are Tips.

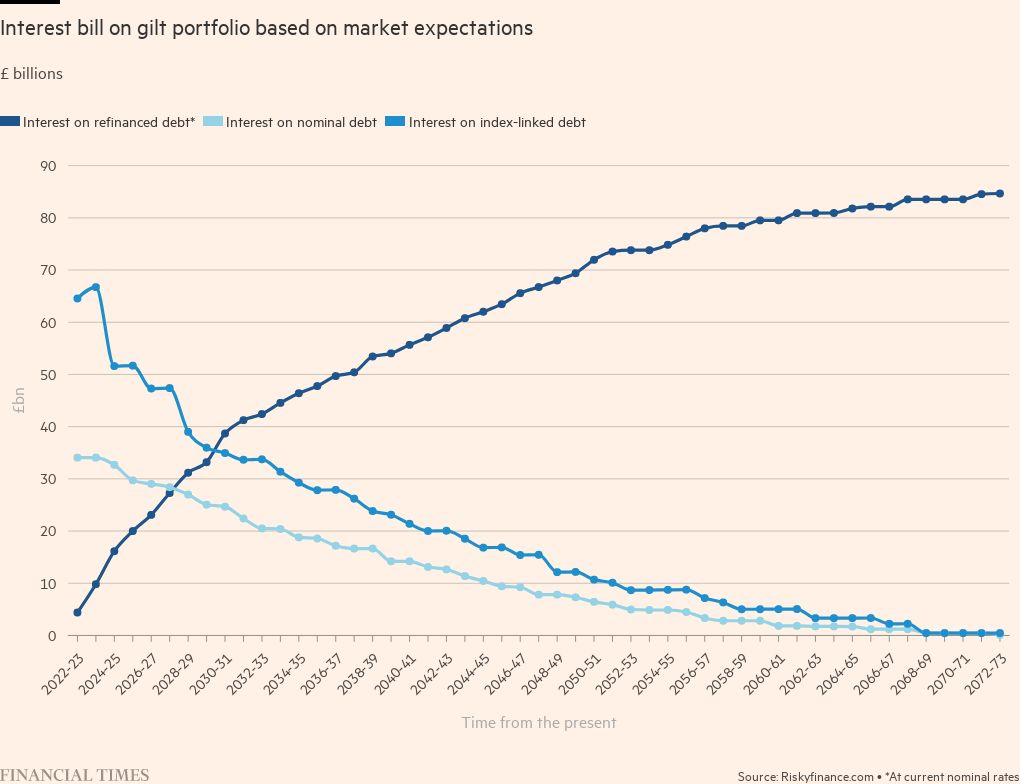

These costs are set to rise further, based on market inflation expectations. We estimate that for the £2tn of UK gilts, annual interest costs are set to rise to £110bn a year in 2024, and stay at around £100bn annually for a decade. That’s double UK government forecasts and doesn’t take into account any additional borrowing.

With the UK government under new prime minister Rishi Sunak about to make difficult decisions about spending and taxation, debt interest becomes more important since it contributes to deficits. Why are inflation-linked bonds proving so expensive? It’s partly due to accounting reasons.

From a cash perspective, linkers look attractive to issuers because of the way investors are compensated for inflation. The annual coupons that characterise most bonds are there, but they are small. The real meat of linkers is in how inflation affects their principal amount or redemption value. Every year this increases by inflation — the so-called “uplift”.

As a result, the UK’s stock of index-linked gilts, which started out with a total face value of £500bn, are now worth £700bn. But the difference doesn’t have to actually be paid to investors until the day the bond matures, which might be decades into the future.

However, this doesn’t satisfy those who compile national accounts, which in the UK is the ONS. Even though no cash is paid to investors before maturity, they do still receive something — the increase in value. Similar to the way that tax authorities like to record grants of unvested employee share options as a form of taxable income, the ONS and other countries’ government bean counters use an “accrual” basis, treating linker uplift as an effective interest payment to investors.

For the years when inflation was low, this didn’t matter — but that’s changed. For forecasts, the ONS defers to the UK Office of Budget Responsibility. In March 2022 the OBR predicted an £83bn interest payment bill for the government over the next 12 months, net of £12bn it receives from the Bank of England’s portfolio of bonds bought under its quantitative easing programme to support markets. The problem is that the OBR’s inflation forecast assumes that the BoE’s Monetary Policy Committee hits its target. As a result, it expects the UK consumer price index to rapidly revert to mean levels after 2023, reducing interest costs on linkers.

Things look different if you use a market-based metric — the break-even inflation rate, or difference between nominal and real bond yields at a given maturity.

In contrast to the OBR, the market does not believe that the MPC will control inflation in the medium term. Break-even inflation is currently around 4 per cent per annum for 10 years, and we use this to compound the value of linkers over time, and thus estimate an annual interest cost. For maturing debt, we assume that this is replaced by new nominal gilts paying the current 10-year yield as a coupon — now 3.91 per cent.

The combination of persistent inflationary uplift and higher refinancing costs will keep UK interest payments at an annual £100bn for years to come. This shows the impact of persistent inflation and government fiscal errors on the long-term financing position of the UK. Other countries with index-linked debt beware.

Comments