The mutual fund at 100: is it becoming obsolete?

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

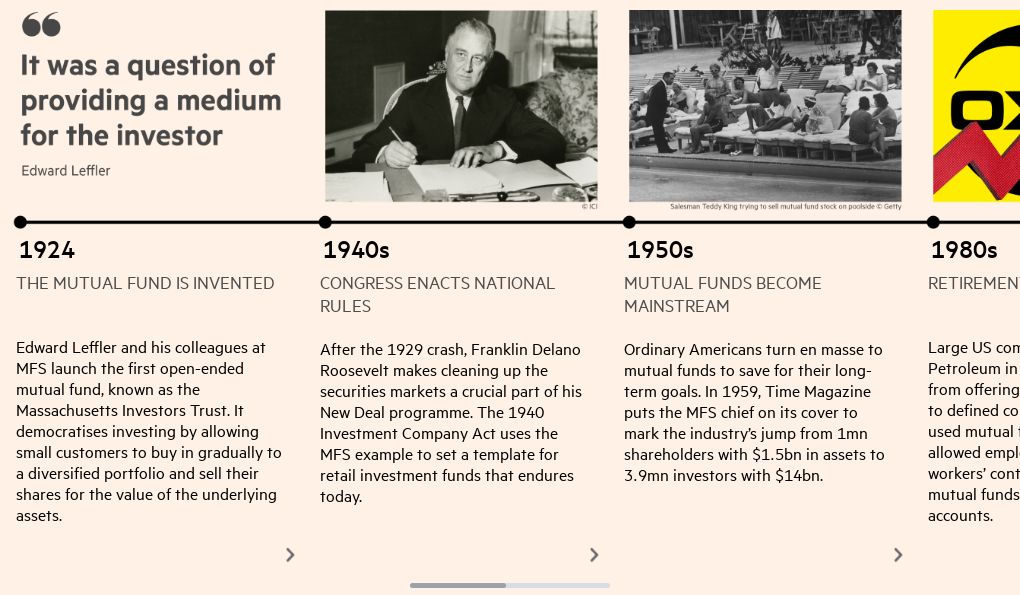

One hundred years ago on Thursday, Edward Leffler, a former door-to-door salesman of pots and pans, revolutionised financial markets. His invention, the open-ended mutual fund, allowed retail customers to buy into a diversified portfolio of stocks and be confident that they would get a fair value when they wanted their money back.

Leffler’s innovation gave lower and middle class people an ownership stake in American capitalism. It also spawned financial titans like Fidelity and Vanguard and thousands of smaller competitors that together employ hundreds of thousands of people.

Mutual funds manage nearly $20tn in US assets and about $63tn worldwide, including everything from stakes in fledgling tech start-ups to government bonds. More than half of all American households and 116mn of the country’s 333mn residents hold shares in at least one mutual fund.

“The mutual fund has democratised investment. It has made investing accessible to the average person in an incredibly durable way,” says Jody Jonsson, vice-chair of Capital Group, the world’s largest active fund manager.

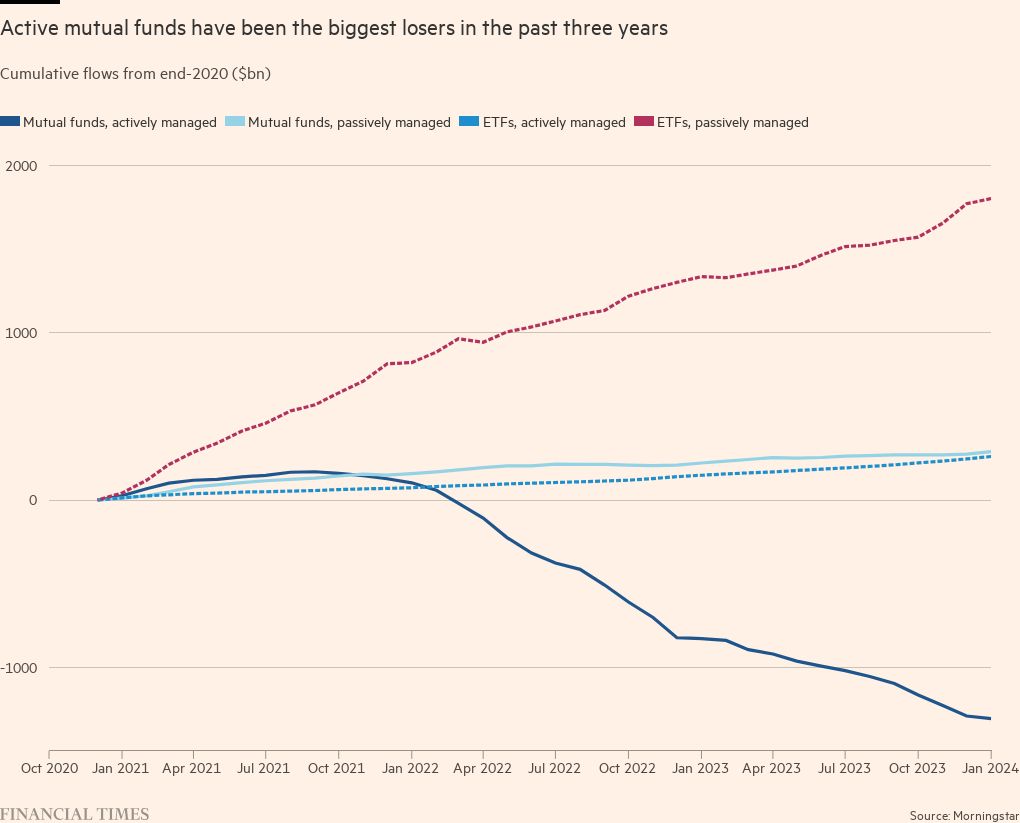

Today, the mutual fund’s dominance is under threat from newer rivals that promise tax advantages, lower fees and rapid trading. US mutual funds suffered more than $1tn in net outflows from January 2021 to December 2023. While they gathered about $13bn in net inflows in February, it was the first time they had a positive month in two years, according to Morningstar, a data group.

The active stockpicking funds that have been the industry’s bread and butter have suffered the biggest decline as a newer option, exchange traded funds, amassed more than $2tn in inflows in the US since January 2021, including more than $575bn last year alone.

Some industry observers predict that the glory days are ending. US money managers showed the world how to help ordinary people share in modern public markets. But as the mutual fund celebrates its 100th birthday, many investors want something faster, cheaper or just different. Unless asset managers adapt, many of them — and one of the most successful financial products of all time — could slowly slide into irrelevance.

“It’s inexorable,” says John Rekenthaler, who has been tracking mutual funds for Morningstar since the 1980s. “I don’t see what a mutual fund can do better than [an] ETF . . . It’s a better mousetrap . . . Eventually the mutual fund is dead.”

Money managers who have spent generations building businesses based on mutual funds contend they will survive and even thrive because investors like and understand the product. It also continues to have advantages in specific areas such as small company stocks and retirement savings.

“There’s a huge, huge population in America that loves the mutual fund for its simplicity,” says Carol Geremia, president of MFS, Leffler’s old company. “We don’t need all of this over-engineered stuff when you think of 30 years and somebody’s retirement. It’s an amazing vehicle that still does that job.”

Even so, the alternatives to mutual funds have fundamentally reshaped the investment marketplace, as customers opt not just for ETFs but also separately managed accounts and collective investment trusts. The shift has made BlackRock the largest asset manager with $10tn in assets and forced longtime stalwarts including Fidelity, Capital Group and Pimco to adapt to stay successful.

“It’s a melting iceberg,” says Jonathan Godsall, a McKinsey consultant, adding that all of his asset management clients are debating what to do about mutual funds. “The question is whether the pace of change will speed up.”

Mutual funds through the years

To understand the significance of Leffler’s brainwave, picture the financial world as it existed in 1924. Stock and bond markets were booming, but so were financial scams. Ordinary Americans wanted to participate, but found individual stocks and bonds too expensive. Many ended up giving their money to unregulated investment pools, which often refused to say what assets they held and offered no guarantee that participants would be able to exit when they wished. Many ended up being wiped out.

“We got here because there was a fundamental recognition that the system was unfair. The little guy wasn’t getting the investment returns of the equity markets,” explains Jenny Johnson, chief executive of Franklin Templeton, a $1.5tn asset manager.

Leffler, who switched from selling pans to securities after the first world war, set out to change all that. Wealthy Britons had been using investment trusts since the 1870s, but MFS made diversified investments accessible to the masses. Its first fund not only allowed small investors to buy in gradually to a regularly disclosed portfolio but also let them sell back their shares whenever they wanted, at the value of the underlying assets.

Competitors such as Wellington and Capital Group quickly followed suit. “The Vanguard Wellington fund goes back to 1929, and one of the reasons that product [has] survived . . . is because it was a balanced, diversified portfolio,” says Rodney Comegys, who heads Vanguard’s equity investment group. “So when the market crashed in the Depression, the fund survived. That’s the power of the mutual fund.”

After the Depression, Congress gave the structure the national stamp of approval with a 1940 funds law that remains the template for US retail investment funds today. By 1959, Time Magazine had put the MFS chief executive on its cover to illustrate a story about mutual funds, calling them “the fastest-growing, most competitive and most controversial phenomenon of the US financial world”.

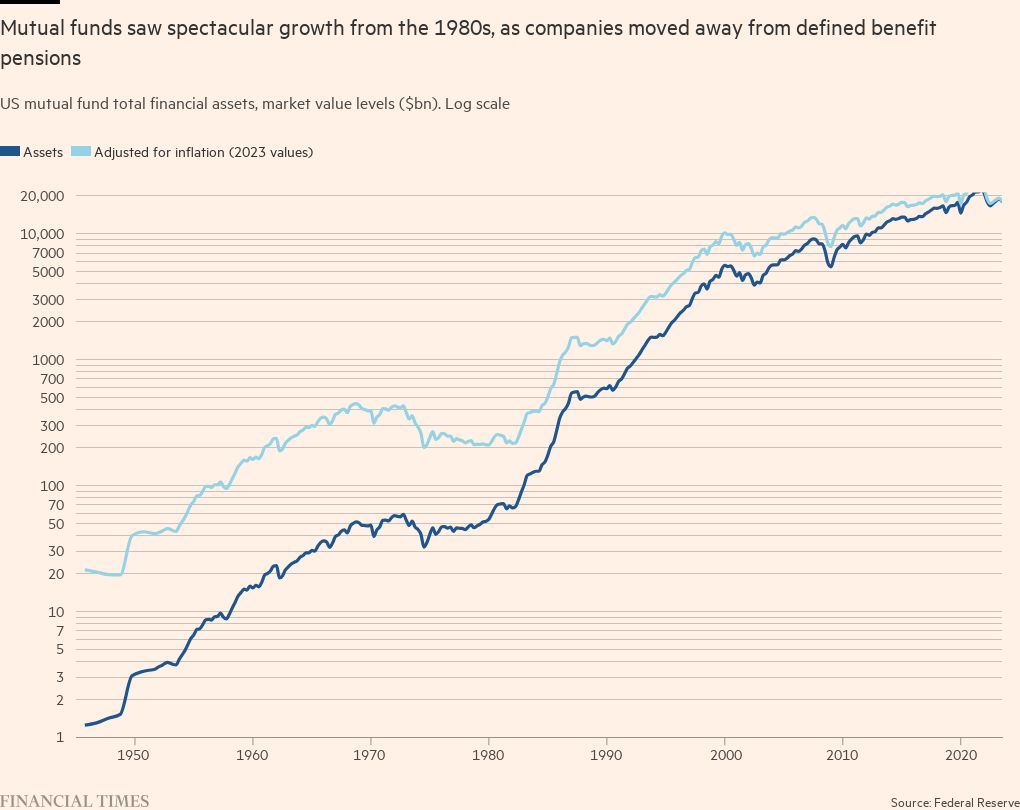

Mutual funds got another boost in the 1980s, as big companies started shifting away from defined benefit pensions. Instead, employers offered to match their workers’ contributions to a slate of mutual funds inside a tax-advantaged retirement plan, usually known as a 401(k) after the relevant section of the tax code. By the year 2000, Fidelity, then the biggest fund company, was managing nearly $1tn, and US mutual funds as a whole had climbed to $7tn in assets.

“Mutual funds allowed more people to get into the market,” says financial historian Richard Sylla of New York University. “The financial industry is an unsung hero; it’s one of the reasons Americans are so rich.”

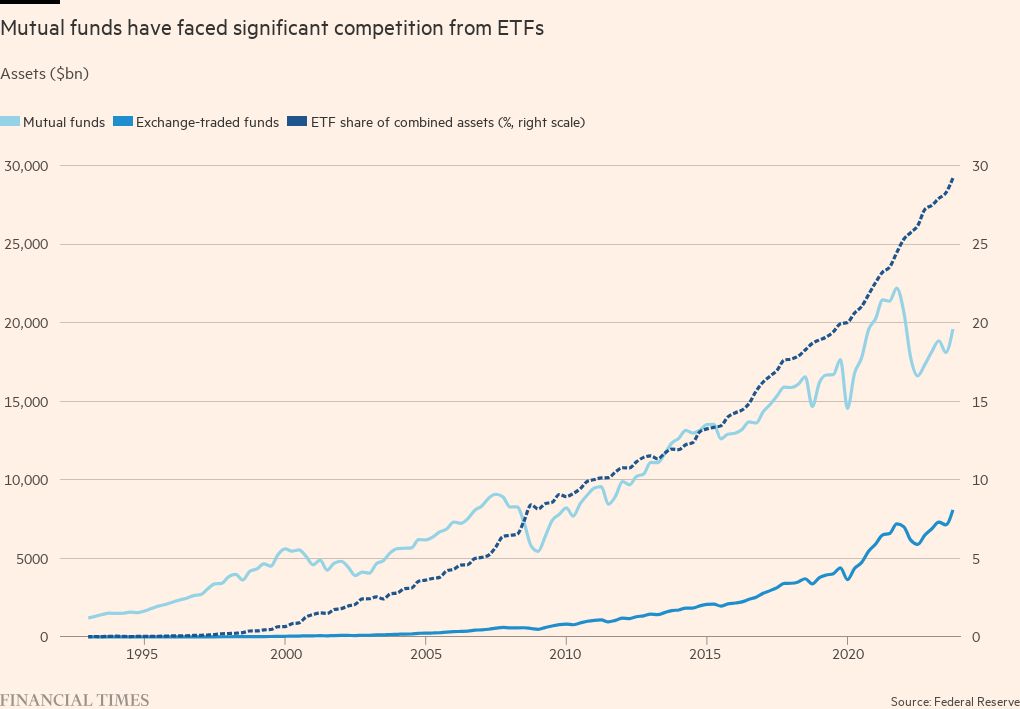

The challenge to mutual fund dominance has been brewing since State Street launched the very first US ETF in 1993, an S&P 500 tracking fund known as SPY that now has $500bn in assets.

For investors, ETFs are like mutual funds on speed. Instead of pricing the pooled assets once a day, as mutual funds do, ETFs trade continuously on exchanges as stocks do. They can keep up this frenetic pace because shares are sold through online trading platforms, and financial firms create and redeem shares with in-kind baskets of securities, rather than having to buy and sell the underlying assets.

That structure attracts frequent traders who want to bet on market movements or the price of specific assets such as gold or bitcoin and also gives ETFs distinct advantages in the competition for long-term investors. ETF sponsors do not have to invest in the same level of back office customer service, so their costs can be lower than traditional mutual funds. And due to a quirk of the US code, ETFs avoid the annual capital gain tax charges that buy-and-hold mutual fund investors incur when they invest outside a retirement plan.

That put ETFs in pole position as the rapid rise of passive investing saw investors abandon active managers and pour money into low-fee products that track specific indices. Tracker funds now account for more than half of all US pooled investments. The three largest US ETF providers — BlackRock, Vanguard and State Street — have amassed commanding market shares predominantly through broad-based passive products.

“In a world where you have zero commission stock trading and can get exposure to a diversified basket of stocks through direct indexes, it’s hard to say that the mutual fund is an efficient vehicle anymore,” says Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management.

ETFs also benefited as retail investors gravitated towards financial advisers. Because they charge management fees on top of those levied by the funds they recommend, financial advisers are under pressure to keep total costs down. “The end customer clearly doesn’t want to pay twice and they want to pay less. Advisers are more apt to direct people into things that are exchange traded,” says Robin Foley, head of fixed income at Fidelity.

Mutual funds lost another advantage in 2019, when the Securities and Exchange Commission removed cumbersome permitting requirements and made it easier for active fund managers to enter the ETF market. That opened the floodgates, as latecomers with sizeable mutual fund franchises began pouring in.

Between 2014 and today, US ETF assets quadrupled from $2tn to $8tn, according to the Investment Company Institute. While that total is still well shy of the $19.6tn in mutual funds, ETFs are closing the gap, powered by popular new products, such as February’s launch of the first ever spot bitcoin ETFs.

There are also secondary challenges brewing from other pooled accounts that cater to very wealthy people and institutional investors. Separately managed accounts grew from about $856bn at the end of 2014 to $1.7tn by 2022, while collective investment trusts nearly doubled from almost $2.4tn to more than $4.6tn in that time, according to Cerulli data.

Many asset managers are scrambling to adjust to client demands. Nearly 2,000 ETFs launched in the US between 2019 and 2023, nearly double the 1,100 new mutual funds, according to Morningstar. Capital Group launched its first ETFs in 2022, Pimco recently filed its first ever request to convert a mutual fund into an ETF, and Dimensional Fund Advisors joined the top 10 US ETF issuers, despite having no offerings in the sector prior to 2020.

“Any company that is disproportionately exposed to the [non-retirement] mutual fund world needs to seriously invest in their capabilities beyond mutual funds or they will face long and persistent headwinds,” says Eric Veiel, head of global investments at T Rowe Price.

Mutual funds may be losing popularity, but that doesn’t mean they are going away anytime soon.

There is so much long-term money already tied up in existing funds that it would take decades, or even generations for it to slip away. More than $10.4tn is in US defined contribution pension plans, and another $5.8tn is in individual retirement accounts, per the ICI. None of that money can be withdrawn without incurring large penalties until the owners reach their 60s.

Furthermore, mutual funds remain the top vehicle for US workers who are saving for future retirement. Most large 401k and other retirement accounts are already set up to use mutual funds, and within such accounts, there is no particular tax advantage to using an ETF. “I don’t actually think the mutual fund is dead. I think the mutual fund is now a retirement vehicle,” says Dave Nadig, who helped design some of the first ETFs in the 1990s.

While some employer-sponsored plans have added ETF options, others are reluctant to offer them, because daily liquidity sends the wrong message about what the savings are for. “If you’re trading your retirement plan intraday, probably your adviser will grab you by your lapels and say ‘please stop’,” said Jeremy Senderowicz, an attorney with law firm Vedder Price.

The headwinds for mutual funds have also been much stronger in equities than in other types of assets.

Fixed income mutual funds suffered only $85bn in outflows between January 2021 and the end of last year, because money pouring into passive bond funds offset most of the departures from active mutual funds, according to Morningstar. And money market funds, which use the same structure as investment mutual funds but compete with banks for cash savings, currently hold an additional $6tn in assets, an all-time high. Asset managers also say the mutual fund structure works better than ETFs for giving smaller investors access to alternatives, such as private equity and private credit, which have been growing in popularity.

Even within equities, US asset managers say mutual funds retain significant advantages in areas such as international and small company stocks. Unlike ETFs, mutual funds can be closed to new investment before they get too large to manage and they only have to disclose their holdings periodically. That makes it easier for stockpicking mutual funds to buy and sell investments without tipping off rivals and high-frequency traders.

“If I’m a small cap manager, I want to get my capacity before I tell the world what I’m investing in, because the world is going to front-run me and . . . move the market away from me. So that’s a real disadvantage to an active ETF,” says Johnson of Franklin Templeton.

In one sign of the durability of mutual funds, Betterment, an online investment platform that primarily dealt in ETFs since its 2008 inception, this month is rolling out software that allows some clients to manage mutual funds as well. The change was necessary to attract financial advisers whose clients already have money tied up in the older products, and those that want to use products that are not available as ETFs, says CEO Sarah Levy, adding: “If this is what advisers believe is best for their clients, we want to be able to support them.”

The situation is also quite different outside the US. While investors in Canada, South Korea and South Africa are keenly interested in active ETFs, those in most other countries remain focused on products structured like US mutual funds. That’s partly because ETFs do not carry the same tax benefits outside the US and suffer from a disadvantage in countries such as Spain. Moreover, mutual funds were never as dominant outside the US, so they still have room to grow. In 2022, just 23 per cent of new European fund launches were ETFs, compared to 70 per cent in the US, according to Oliver Wyman.

The divergence will protect mutual funds from extinction, but it is also forcing money managers to deliver their investment strategies in many different packages. “This breaking down of the strategy and wrapper combination is very important. Clients are going to want to consume strategies in multiple different ways,” says Stephen Cohen, BlackRock’s chief product officer.

Even MFS, the original mutual fund pioneer, is not immune. Outgoing chief executive Mike Roberge says the firm is poised to launch its first ETF as early as this year.

After generations of offering a prix fixe menu, the most successful asset managers are shifting to a buffet.

Data visualisation by Keith Fray

Comments