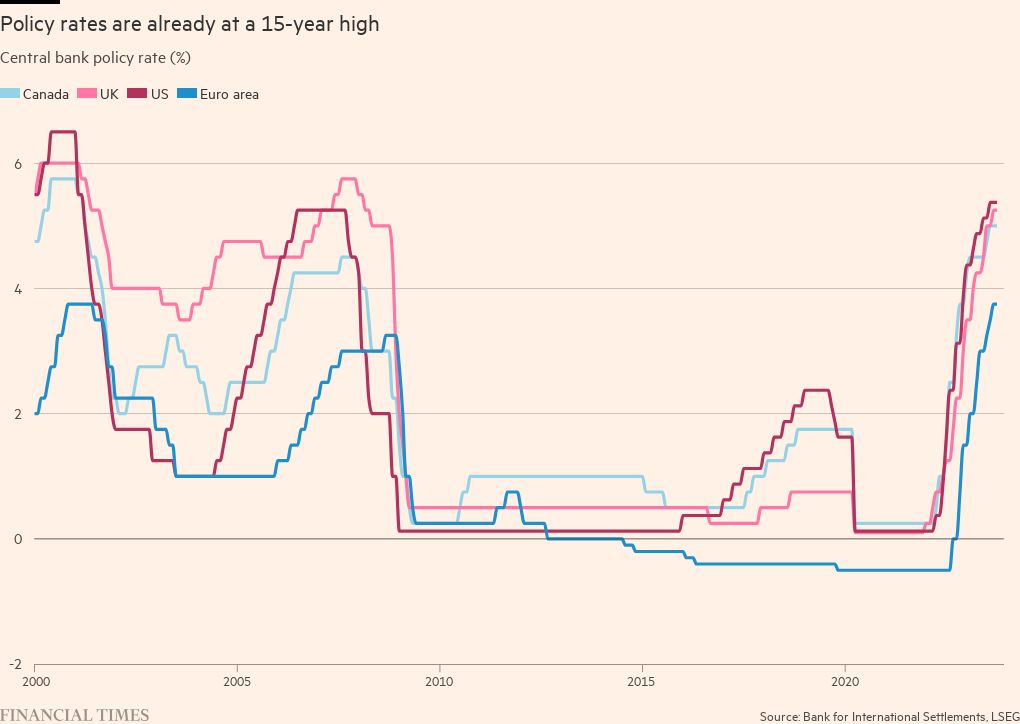

Central bankers split on whether war-related energy price jump would fuel rates

Simply sign up to the Global inflation myFT Digest -- delivered directly to your inbox.

Central banks are at odds over how to respond to a possible jump in energy prices should the Israel-Hamas war escalate.

While rate-setters have conventionally ignored volatility in the energy markets, central bank heads in Canada and the UK have signalled they would need to address the inflationary risk of higher oil and gas prices.

Tiff Macklem, governor of the Bank of Canada, told the Financial Times that the after-effects of energy price shocks could prove more challenging to control because of the recent wave of inflation — the biggest such leap in a generation.

“When you have been above [your inflation] target for two years, expectations are above target and businesses are passing through input costs quickly, you have to be more cautious,” he said.

“If you have higher transportation costs . . . passing through the higher fuel price to the prices of other goods and services, that would be a sign we have more work to do.”

Such arguments contrast with some central bankers’ previous insistence that energy price rises — which are not easily countered by interest rate rises — have only a transitory impact on inflation.

In its inflation outlook published last week, the BoE also listed the Middle East and energy as one of the “upside risks” to price stability. Speaking on that occasion, BoE governor Andrew Bailey said the world had been through a “succession of big supply shocks with no gaps between them”.

But Christine Lagarde, the head of the European Central Bank, struck a different tone after the bank kept rates on hold at its policy meeting late last month.

The eurozone was, Lagarde said, “a completely different economy today”, compared with when energy prices surged last year as EU countries weaned themselves off Russian imports. Higher rates and weaker demand this time round would constrain any price pressures emanating from the Middle East.

Another member of the ECB’s rate-setting governing council was more cautious, telling the FT that the response to rising oil prices would depend on the cause.

The ECB rate-setter drew a distinction between market tensions, which could be safely ignored, and a more problematic full-scale supply shock, such as if Iran were to attempt to close the Strait of Hormuz, through which a third of liquefied natural gas and a quarter of oil is transported.

A major event like this would raise parallels with the 1973 Arab oil embargo against the US, which quadrupled crude prices. So far, prices remain below the level of October 7, the day of the Hamas attack on Israel.

A jump in energy prices almost immediately raises headline inflation. But in economies where demand is depressed, more expensive oil and gas could eventually weaken price pressures by weighing on earnings and output.

However, in economies where demand is strong, higher energy costs can seep through to other areas of the economy as workers and companies raise the cost of their labour and products.

Despite relatively buoyant growth in the US, Federal Reserve chair Jay Powell last week appeared relaxed.

Global oil prices had not reacted too significantly to the conflict thus far, he said, and it was not clear if it would have “significant economic effects”. Of critical importance was whether the conflict broadened out.

Others at the Fed are more concerned. On Tuesday, Michelle Bowman, one of the more hawkish governors, warned of the risk that higher energy prices could “reverse some of the progress made to bring overall inflation down”.

Bowman expected the Fed to need to increase interest rates “further” to get inflation all the way back down to its 2 per cent target, saying she would support such a move “should the incoming data indicate that progress on inflation has stalled or is insufficient to bring inflation [down]”.

As it stands, markets do not expect the conflict in the Middle East to affect global interest rates.

Marcelo Carvalho, global head of economics at BNP Paribas, said the bank expects the oil price to hover at about $100 for a barrel of Brent. At that price, central banks would still look through the shock. Only in an adverse scenario, where oil prices surge towards $120, would policymakers start to fret.

“If you were talking about an oil shock a year or two ago, when things were really hot domestically, inflation was going higher, expectations were getting out of hand, food prices were increasing, rates were very low . . . that would be more worrisome for central banks,” he said.

“Now, rates are much higher, you have some signs of moderation in activity and you have very clear signs of declining headline inflation.”

Comments