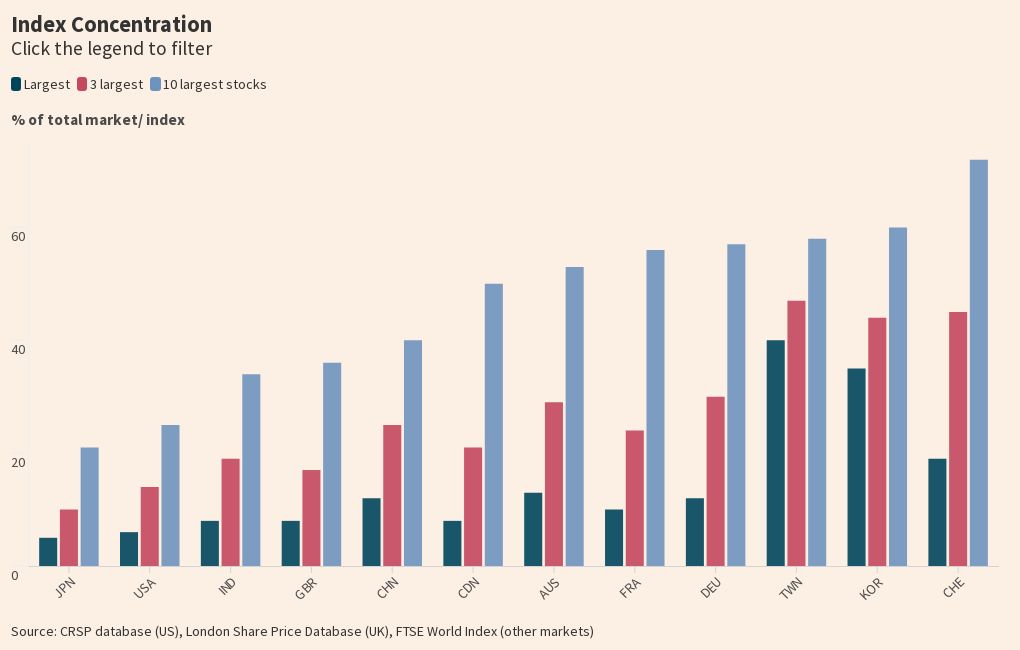

The US equity market is one of the least concentrated in the world

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

We’re not entirely sure whether it was BofA’s Michael Hartnett or Mike O’Rourke from Jones Trading who coined the term ‘Magnificent Seven’. Frankly, it doesn’t really matter. What does matter is that it has become increasingly hard to discuss equity markets without reference to the moniker.

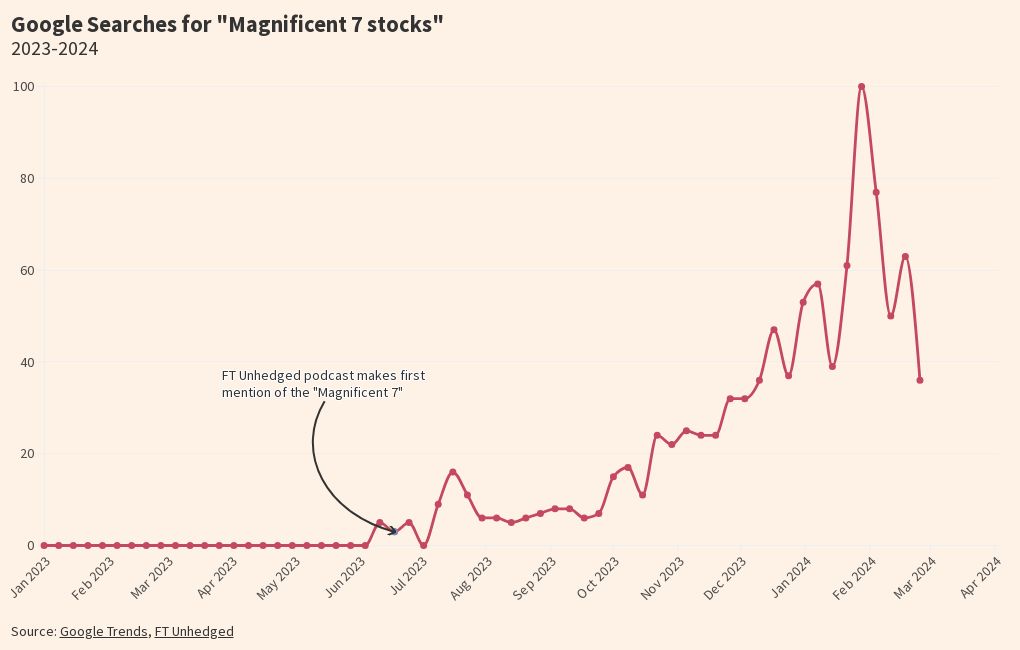

Magnificent Seven was Katie Martin’s Year in [two] word[s] 2023, and has been mentioned in 211 FT articles over the past twelve months. As a proxy for worldwide interest in the stocks, here’s a chart of Google searches for the “Magnificent 7 stocks”.

You’d be forgiven for thinking that the rise and rise of a few successful firms was cause for celebration. But it has given a lot of people the heebie-jeebies. After all, having maybe 30 per cent of your entire stock market’s capitalisation tied up in a small handful of companies doesn’t feel massively diverse.

And — as a chart borrowed from Duncan Lamont at Schroders shows — the extent of concentration in the S&P 500 is not something investors are used to.

So it was fascinating to see this chart in the latest edition of the Credit Suisse UBS Global Investment Returns Yearbook 2024 (a summary edition of which is available online):

The data looks a little different to Schroders’, perhaps due to timing or index selection. But the point is this: rather than showing the US up as a dangerous outlier in the world of index concentration, only Japan is less top-heavy as a market (albeit among their selection of countries).

Of course, the reason folks don’t get as angsty about Taiwanese or Korean stock concentration is that most global managers own maybe one Taiwanese stock or one Korean stock. But with the US hogging over 60 per cent of global equity benchmarks, concentration of market capitalisation in US stocks feels like — and is, for the average global investor — a bigger deal. Indeed, as Lamont observes, the top ten US stocks account for as much of the MSCI ACWI market cap as all Japanese, UK, Chinese, French and Canadian firms put together.

The UBS reports’ authors — academics Elroy Dimson, Paul Marsh and Mike Stanton — are explicit in their ambition to better-arm today’s investors with the lessons of the past, and to broaden analysts’ perspectives beyond a narrow US market focus. While there are certainly reasons why the Magnificent 7 might not continue to eat the world, the study is a refreshing antidote to any analysis that relies on an iron law of intra-market gravity to bring down US stock concentration.

Comments