Autumn Statement: What it means for your money

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Barely eight weeks since the disastrous “mini” Budget, chancellor Jeremy Hunt has delivered a package of tax rises and spending cuts designed to repair Britain’s battered public finances — but it comes at a cost to the nation’s personal finances.

Promising to protect the vulnerable and concentrate tax rises on those with the broadest shoulders, the chancellor warned the UK economy had already entered recession, and that things would get worse before they improved.

Here is a summary of the key measures likely to affect your own personal finances:

Tax

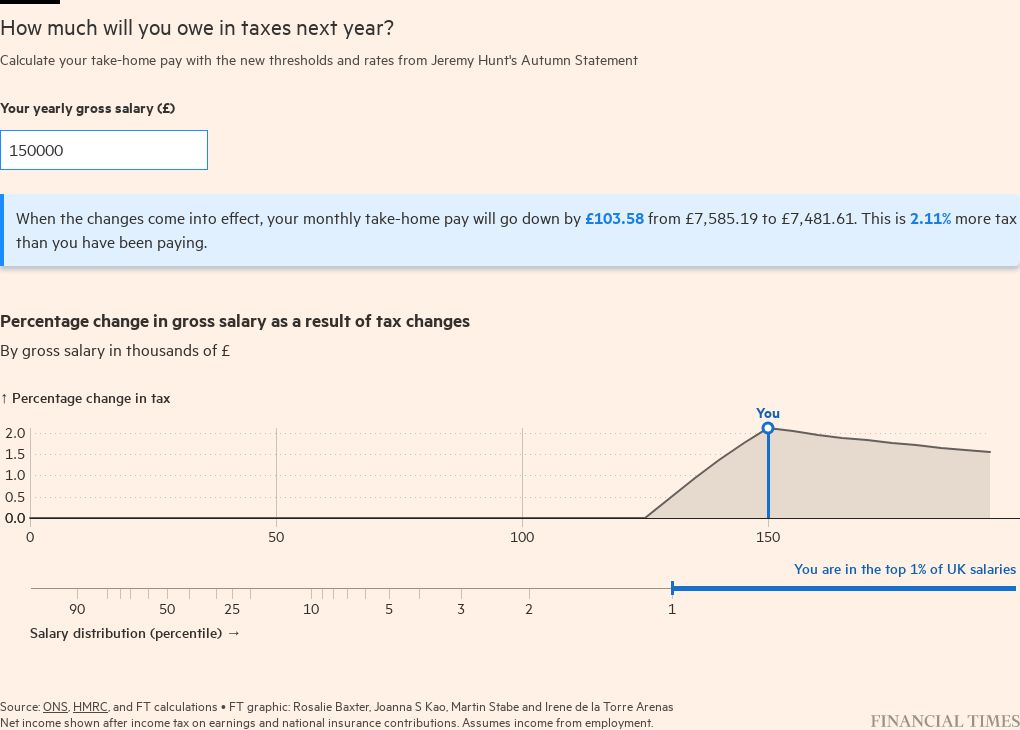

Around a quarter of a million taxpayers with an income above £125,140 will pay the 45p top rate of tax from next April, after Hunt lowered the threshold from its existing level of £150,000.

This means people with an income above £150,000 will pay an extra £1,243 in income tax per year.

“We are asking more from those who have more,” the chancellor said.

He also extended the freeze in other income tax and national insurance thresholds for a further two years until 2028, which is expected to raise tens of billions of pounds in “stealth taxes” as inflation pushes up workers’ pay.

Rather than rise in line with inflation, the tax-free personal allowance will remain at £12,570 and the higher-rate threshold at £50,270 in England, Wales and Northern Ireland (Scotland has different tax thresholds).

The freeze is expected to drag about 3mn people into paying higher rates of income tax by 2026, according to analysis by the Institute for Fiscal Studies.

The freeze to the inheritance tax “nil-rate band” will also be extended from 2025-26 to 2027-28, in a move that could raise at least half a billion pounds for the Treasury.

Local authorities will be able to raise council tax bills by up to 5 per cent from next April without the need to hold a referendum.

The married couple’s allowance is set to rise in line with September’s inflation figure of 10.1 per cent from next April.

From April 2025, electric vehicles will no longer be exempt from vehicle excise duty.

Investments

The chancellor announced plans to substantially reduce tax-free allowances that benefit investors.

Capital gains tax allowances will be pared, with the annual tax-free allowance slashed from £12,300 to £6,000 from next April, halving again to just £3,000 from April 2024.

The tax-free dividend allowance will be halved from £2,000 to £1,000 from next April, and halved again to just £500 from April 2024.

Expected to raise more than £1.2bn a year from April 2025, the measures will hit investors who hold income-paying shares outside tax wrappers like Isas and pensions, as well as costing limited company directors who are remunerated through dividends.

“Whilst high net worth individuals are unlikely to feel much pain from this, for many small investors, that increase in tax on dividends and capital gains is going to be significant,” said Charles Incledon, director at Bowmore Asset Management.

“Cuts to this income could cause a real squeeze on the finances of many small investors, especially those who are retired and depend on dividend income from their shares. Bad news considering that we have a cost of living crisis at the moment.”

However, fears that the chancellor would go further and align capital gains rates with income tax rates proved unfounded.

Pensions

The triple-lock on the state pension was maintained, meaning a 10.1 per cent boost for pensioners next April.

The full annual amount of the new state pension will rise above £10,000 for the first time next year, and will be worth over £200 per week.

Pension credit, a benefit received by the poorest pensioners, will also be uprated by 10.1 per cent.

However, the chancellor said a review into the current level of the state pension age would be published in “early 2023”.

State pension age has been gradually increasing for men and women, and will reach 67 by 2028. Treasury documents said the review would “carefully balance important factors, including fiscal sustainability, the economic context, the latest life expectancy data and fairness both to pensioners and taxpayers.”

The lifetime allowance governing what can be saved tax-free into a pension had already been frozen at £1.07mn until 2026, but Treasury documents did not stipulate whether the freeze would be extended until 2028.

Cost of living payments

From next April, the current package of help measures with energy bills will be more targeted at the lowest-earning households.

Currently, the energy price guarantee caps energy bills for the average home at £2,500 per year. From next April, this cap will rise to £3,000, and remain at this level for 12 months, saving the government £14bn.

The £400 support package received by all UK households will not be repeated next year, but households on means tested benefits will receive a cost of living payment worth £900, pensioner households will receive £300 and those with disabilities £150.

Households using alternative fuels such as heating oil will see support this winter doubled from £100 to £200.

The government may “revisit the parameters” of the scheme if wholesale energy costs increase substantially. It will also consult on measures to cap the amount of state support that large energy users can receive from April 2023, but would seek to protect vulnerable people with high energy needs.

The help measures will be partially funded by higher windfall taxes on energy companies.

The chancellor confirmed that means-tested benefits would also rise by 10.1 per cent next April, and the and the national living wage by 9.7 per cent.

Property

There were no changes to stamp duty — one of the few “mini” Budget measures to have survived intact.

However, the chancellor said these measures will only remain in place until March 31 2025.

Former chancellor Kwasi Kwarteng doubled the threshold at which stamp duty would begin to apply in England and Northern Ireland to £250,000.

First-time buyers were also exempted from paying the tax on the first £425,000 of their purchase, up from £300,000.

Hunt said that change would now be temporary, “creating an incentive to support the housing market and the jobs associated with it by boosting transactions during the period the economy most needs it”.

Additional reporting by George Hammond

Autumn Statement: expert reaction

Nimesh Shah, chief executive of accountancy group Blick Rothenberg

The “squeezed middle” were squeezed again by Jeremy Hunt. The extension of Rishi Sunak’s “big freeze” of the personal tax allowances and thresholds to 2028, and reduction to the 45 per cent income tax threshold to £125,140 continues to expose the middle to higher rates of taxation. The inflationary impact, the cuts and freezes to tax allowances and thresholds and the limited government support for the middle earners suggests that those with the not-so-broadest shoulders are bearing the most severe burden.

Anna Bowes, co-founder of SavingsChampion.co.uk

Although it’s possible there will be an update in next year’s Budget, I expect the Personal Savings Allowance and the Individual Savings Account allowance will both remain the same in 2023-24. The PSA has been ignored since inception.

This allowance means that basic rate taxpayers pay no tax on the first £1,000 of savings interest; for higher-rate taxpayers it is £500; and additional rate taxpayers receive no allowance at all. Last year, the best easy access account was paying about 0.5 per cent, which meant a basic rate taxpayer would only breach the allowance with a deposit of £200,000. Today, with the best account paying 2.81 per cent, it will be breached with just £35,587.

Christine Ross, client director at Handelsbanken Wealth & Asset Management

This was not an event for savers. More than ever it is important to remember: if you don’t use it you lose it. The capital gains tax allowance remains at £12,300 for the rest of this tax year before dropping sharply in the next two tax years. Many savers sell investments annually from a taxable portfolio and reinvest the proceeds in their Isa, with any profits absorbed by the CGT allowance.

Any loss realised can be carried forward to future years. This may help to mitigate the effect of the vastly reduced allowance going forward.

At the same time more savings will be efficiently housed in an Isa. This will also help to alleviate the impact of the halving of the dividend allowance next year and again in 2024.

Simon Edelsten, co-manager of the Mid Wynd International Investment Trust and the Artemis Global Select Fund

Did the chancellor offer reasons for investors to back UK assets? It was encouraging to hear plans for energy efficiency and maintained infrastructure spending. But details seem far off and the repeated commitment to net zero targets sits unconvincingly alongside windfall taxes on electricity companies. Strikes and weaker sterling have also been issues. However, there was nothing to address the calls of workers looking to preserve real incomes, nor to persuade us that revitalising sterling is a core objective. Investing in the UK seems to offer modest upside and considerable risk compared with the resilience of the US economy or the growth potential of Asia.

Comments