How Europe can adapt to living without Russian gas for years

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is the founder and chief investment officer of Andurand Capital Management

Russia has historically supplied about 30 per cent of the EU and UK’s gas consumption by pipeline. Those exports have already been cut by 75 per cent. If Moscow stops them entirely, will Europeans freeze to death in the winter, as Russian propagandists have been warning?

Almost certainly not. In fact, it looks as though Europeans have a great deal more capacity in managing the situation than the fearmongers thought.

Much of European gas demand comes from heating. If Europeans just lower thermostats in their homes by an average of 3C — down to 19C this winter — that could make a big difference.

The International Energy Agency estimated in a March report that a 1C move lower in average thermostat levels from 22C in the winter would save 10bn cubic metres of gas in EU and UK demand.

But let’s look at the impact of a 3C reduction by focusing on a group of nine European countries for which data are the most detailed: Germany, the UK, France, Italy, Belgium, Netherlands, Austria, the Czech Republic and Slovakia. In 2021, this EU+ group represented 69 per cent of EU and UK demand.

Rising imports of liquefied natural gas and a switch by industry to using more oil have reduced much of the 2023 deficit caused by the loss of Russian imports.

A reduction to an average of 19C would solve two-thirds of the remaining deficit for these nine countries. And if accompanied by a 5 per cent cut in power usage — which could be achieved by switching it off in unused rooms and buildings — the deficit would disappear.

How uncomfortable would a 3C lowering of indoor temperature be? It would only involve reducing current temperatures of 22C to levels already experienced in recent history.

A 1982 study found the average indoor temperature in the UK was about 16C in 1978. A 1996 study from the UK Department for the Environment, Transport and the Regions found indoor temperatures hovered at about 18C in the winter. Therefore, 19C is not a very high price to pay given what is at stake with Russia’s behaviour.

Furthermore, this inconvenience would have to last only a couple of years, as Europe attracts more of a growing LNG supply while increasing solar and wind power generation.

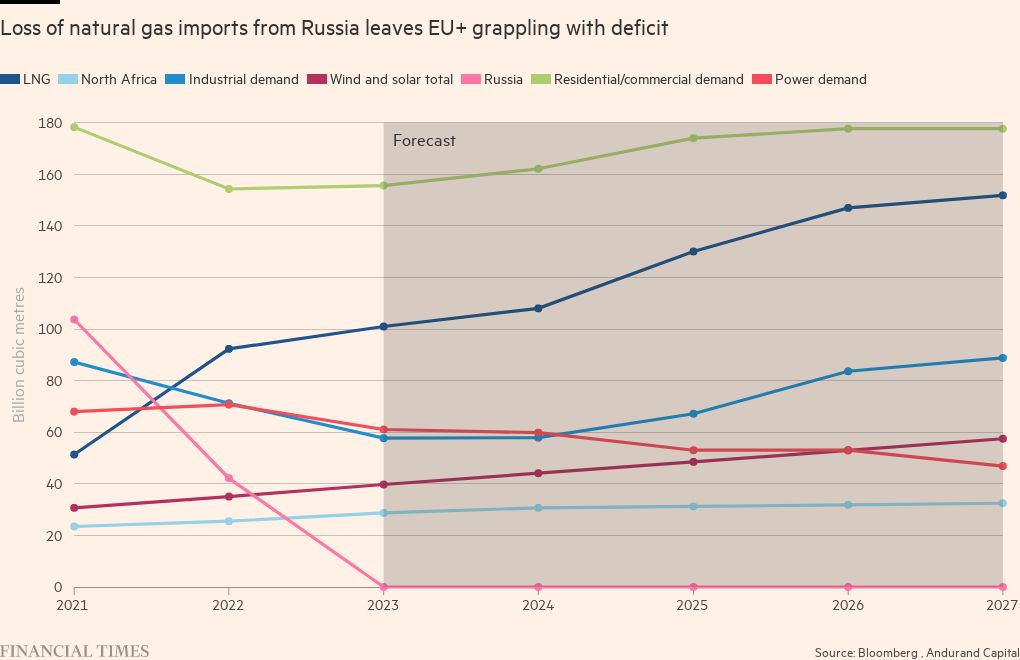

Imports to the EU+ group of natural gas from Russia via pipelines are expected to fall from 103bn cubic metres in 2021 to 42bn cubic metres in 2022 — a drop of 61bn cubic metres. Let’s assume that they fall to zero from October 2022 onwards.

This will be partly offset by LNG imports from elsewhere. These have gone up more than the IEA or other analysts believed possible just a few months ago.

For 2022, the EU+ is expected to import 41bn cubic metres more LNG from elsewhere than in 2021, covering 67 per cent of the expected drop in Russian imports. From 2023 onwards, we can safely assume that the countries will further import between 30 and 50 per cent of global LNG production additions.

Industrial switching has also been way above most analysts’ expectations. The industrial sector in the EU+ group has already switched 35 per cent of its natural gas consumption to oil. Additional wind and solar power capacity is expected to help displace 3bn cubic metres a year of natural gas, with the potential to expand more.

But this is still not enough to avoid natural gas shortages going forward. Without any further demand reduction, a deficit is expected for the EU+ group of 28bn cubic metres in 2023 — with Russian supply down 103bn cubic metres, LNG imports up 50bn cubic metres and industrial switching of 30bn cubic metres to oil. On the IEA figures, a 3C drop in average thermostat levels would cut that by 21bn cubic metres.

In order to avoid social unrest, governments in the EU and UK have chosen to shield consumers from most of the increase in wholesale natural gas prices. As a result, we should not expect a significant drop in customer demand unless there are widespread public awareness campaigns on ways to save energy, such as lowering our thermostats.

The hardest adjustment will be in the coming six months. If Europe can do what is needed to reduce demand, it will have proven both that it is more resilient than thought, and that it can live without Russian gas.

This will take a lot of froth out of the market, and bring significantly lower prices, as the situation will then ease every year. On top of a potential $100bn revenues from natural gas exports to Europe, Russia will have lost much of its ability to blackmail European countries over energy.

Letter in response to this article:

Comments