Why Japan remains the biggest investor in the US

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Early this year, Mazda cars rolled off an American production line for the first time in a decade. Mazda Motor’s new plant near Huntsville, Alabama — a joint project with fellow Japanese carmaker Toyota — began producing a sport utility vehicle designed for the US market.

The U-turn by Mazda, years after it severed ties with longtime partner Ford and bowed out of US manufacturing, shows how much the company relies on US sales. North America has become its biggest profit centre outside Japan, growing to account for 30 per cent of group sales even as Japan’s share has shrunk.

Mazda and Toyota jointly own and operate the Alabama facility, and have together invested $2.3bn in the project. Neither can afford for it to fail.

“Our future growth lies in the US,” says Masashi Aihara, a Mazda veteran who is now president of Mazda-Toyota’s joint venture. “Our fortunes are riding on this resumption of US manufacturing.”

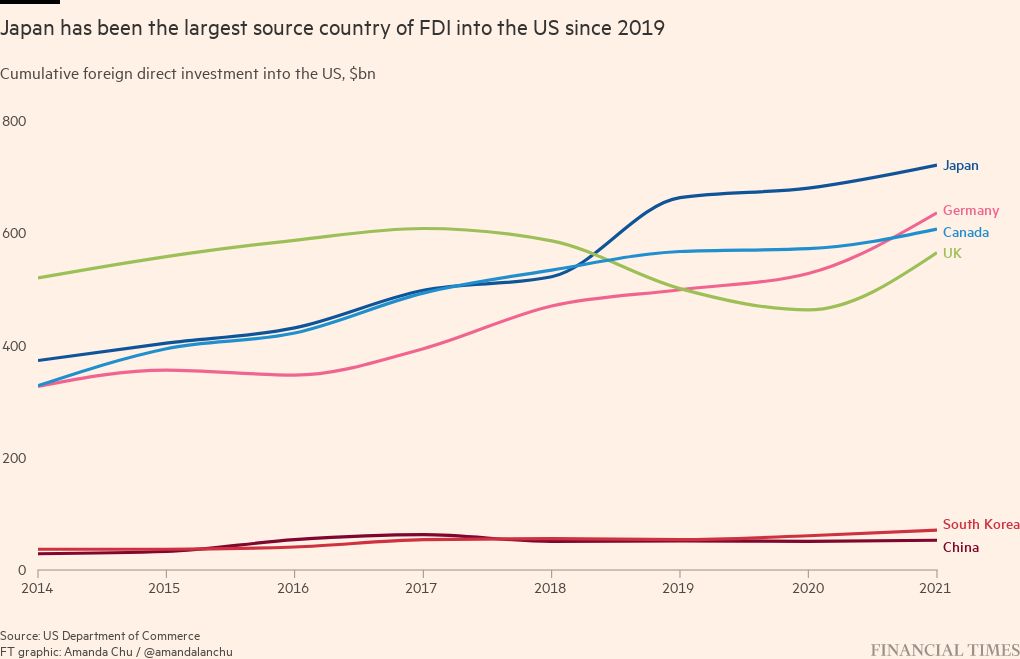

Japan has been the biggest foreign investor in the US for three straight years, as companies chase growth in the world’s richest country. But the market also presents challenges — especially rising costs and cultural differences — that may make some prospective investors think twice.

Japan’s cumulative direct investment in the US reached $721bn last year — 14 per cent of the $4.98tn total, according to data from the US Department of Commerce. American subsidiaries and affiliates of Japanese companies exported $75.3bn worth of goods in 2020 — well ahead of second-placed Germany’s $47.5bn. Their research and development spending totalled $12bn, a close second to Germany’s $12.7bn, and they employed about 930,000 workers, second only to UK companies.

About half of Japan’s investment has been in manufacturing. Besides the car industry, there has been fresh spending in food and pharmaceuticals, tapping into strong US demand. Fujifilm last year announced plans for a ¥200bn ($1.4bn) drugmaking plant in the US.

In the service sector, meanwhile, retail group Seven & i Holdings acquired petrol-station convenience store chain Speedway for $21bn in 2021. It now expects its overseas convenience stores to top their domestic counterparts in operating profit this fiscal year.

“North America is becoming the main driver of our business,” says Ryuichi Isaka, Seven & i’s president.

Japanese companies operating abroad have generally focused on China, south-east Asia and Europe along with the US. The rise in investment in America comes amid concerns about China, which is expected to rival the US market in size but is beset by growing political risks.

These include the punitive tariffs imposed on Chinese imports by Washington, along with increasing Chinese government interference with the private sector. Japan’s direct investment position in China grew only 26 per cent between 2015 and 2021, compared with 50 per cent in the US, according to data from the Bank of Japan.

“Given the business risks, we can’t really hit the gas on our China operations,” an executive at a Japanese carmaker says.

The push by US president Joe Biden’s administration to bring manufacturing and supply chains home has made it difficult for Japanese companies to import parts and materials from China to the US as they have in the past. Businesses looking to expand in the US need to invest more to build up local procurement and production networks.

This expenditure does not guarantee success. Competition is intensifying not only from local players, but also from European and South Korean rivals.

And the US does not necessarily offer the best returns on investment to begin with.

Profit margins on direct investment by Japanese companies have stayed solidly in the double digits in China, with south-east Asia generally not too far behind that at about 10 per cent. But they have long been below 10 per cent in the US, slumping to less than 5 per cent since 2020.

One factor is high costs: in a survey last year by the Japan External Trade Organization (Jetro), a trade promotion body backed by Japan’s government, more than half of Japanese companies operating in the US cited rising wages as a challenge, with nearly as many pointing to increases in logistics and procurement costs.

A further difficulty is the wider range of wages in the US compared with Japan, where deflation has gripped the economy for three decades.

Employee pay tends to vary little under the seniority-based wage structures that Japanese companies typically use, and efforts to introduce merit-based pay have so far done little to change that. But in the US it can be hard to attract outstanding talent without outstanding pay.

Industrial group Hitachi, for example, which is trying to fill engineering and other positions at its digital technology centre in California with the help of a global employee database, says it is “not easy” to share staff between Japan and the US because of differences in remuneration systems between the two countries.

This also applies to management, leading to situations like the head of US-based 7-Eleven making about 20 times as much as the boss of Seven & i, its Japanese parent.

Poor returns on mergers and acquisitions, especially in the finance and telecommunications sectors, also weigh on FDI’s overall profitability. When Japanese companies buy businesses in the US, they often subsequently struggle with integration — overcoming differences in language, culture and corporate climate to align local management with the Japanese parent. The US’s widening political divides can be especially tricky to navigate.

Take abortion. As conservative states ban the procedure, companies face the question of how to support their workers. But Japanese businesses are largely unfamiliar with the Christian cultural background of the debate, and find it hard to unite employees with differing views. A list compiled by Yale University of nearly 140 companies offering abortion-related support includes few from Japan.

Japan’s cautious business culture adds to such difficulties. Companies have historically tended to enter the US market only after their products and services are established in Japan, but size and agility do not necessarily go hand in hand.

Some observers think that doing things the other way around could deliver higher returns. Ralph Inforzato, special adviser to Jetro Chicago, argues that Japanese entrepreneurs should look to the US sooner rather than later. “In 2022, Japanese businesses, especially tech start-ups should consider quickly ramping up their business models in the US first, and then in Japan,” he says.

Comments