A stronger dollar might hit emerging economies harder this cycle

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is head of emerging markets economics at Citi

Developing countries live their economic lives at the mercy of the US Federal Reserve. This may sound blunt, but that makes it no less true.

When US monetary conditions are loose, capital is pushed towards emerging economies, making it easier for these countries to fund themselves. And when the Fed tightens, as it is doing these days, the wave reverses course as capital seeks higher yields back in the US.

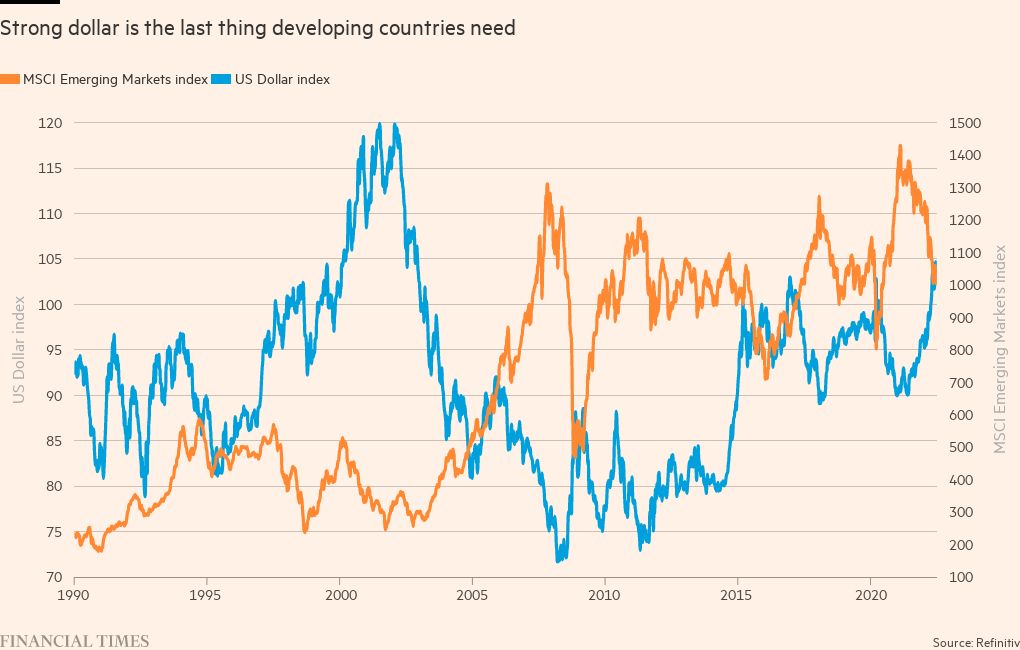

This cycle is usually understood as resulting from the impact of higher or lower US interest rates on capital flows to developing countries. Yet it’s not just the yield on US assets that affects these countries; the dollar exchange rate also plays a big role in this drama.

Here are four ways in which a stronger dollar makes life tough for emerging economies.

First, a stronger dollar tends to depress global trade growth. It is the dominant currency for invoicing and settling a huge swath of global trade transactions. Since the purchasing power of non-US currencies declines when the dollar strengthens, an appreciation of the US currency tends to make the world poorer and less engaged in trade.

Since developing countries tend to be what economists call small, open economies that are especially dependent on global trade, anything that puts downward pressure on that is likely to be unhelpful for them.

Second, a stronger dollar tends to erode the creditworthiness of developing countries that have debt denominated in the US currency. Dollar appreciation makes it more expensive for countries to buy the US currency they need to service their debts. This is likely to be most painful for lower-income countries that typically have only a constrained ability to borrow internationally in their own currencies even at the best of times.

Third, a strong dollar is likely to be inconvenient for China these days, and what’s bad for that country is generally unhelpful for emerging economies given their linkages to Chinese supply chains and commodities demand.

Although it is superficially attractive to think that a weakening renminbi might be a convenient way of boosting Chinese exports, there are two bigger forces at work in the opposite direction.

One is that by driving up the cost of imported commodities, a weaker renminbi makes life tough for small- and medium-sized enterprises in China that in any case have been facing a prolonged squeeze on their profitability. And another is that a weakening renminbi tends to trigger capital outflows from China, something that authorities in Beijing prefer to avoid as they seek to keep expectations on its currency positive.

Finally, a stronger dollar now is likely to be more inflationary for emerging economies than was the case in the past. Recent years have allowed us to forget that currency depreciation in a developing country can quickly lead to inflation. That’s because the so-called “pass-through” from the exchange rate to inflation has indeed tended to be relatively low in recent years.

Yet the past may not be a good guide to the present. One big reason why exchange rate depreciations haven’t proved inflationary in recent years is simply that global inflation was stubbornly low. That’s no longer true. It is worth worrying that at a time when inflation is accelerating, a currency depreciation is more likely to add a kicker to domestic price pressures. Add combustible material to a fire and you get more fire.

The world economy is a fairly hostile environment for developing countries these days: rising recession risks in the west; an uncomfortable slowdown in China; diminished availability and higher cost of funding as investors become more risk averse; accelerating inflation almost everywhere; and increasing concern about the availability of food in a number of countries.

And that’s just in the foreground. In the background, the prospect of de-globalising efforts by policymakers in the US, in Europe and in China to achieve supply chain resilience will come at the expense of future flows of foreign direct investment to emerging economies.

With all this going on, a strengthening dollar is the last thing developing countries need. Yet the problem may not go away soon. In the early 1980s — the last time the US had a truly stubborn inflation problem to deal with — the dollar went up by close to 80 per cent. History may not quite repeat itself, but if the dollar is going to keep strengthening with anything like the ferocity of 40 years ago, the ride will be bumpy for emerging economies.

Comments